Introduction

Teaching kids about money is one of the most important things a parent can do — yet most children reach adulthood without ever learning the basics. When parents prioritize teaching kids about money early, they give their children a head start that pays dividends for life. Too many children are growing up, finishing school, entering the workforce, and arriving at adulthood completely unprepared for one of life’s most unavoidable realities: managing money.

For generations, financial education was treated as something children would simply “figure out” when the time came. But in today’s world, with rising costs of living, easy access to credit, and digital payments that make spending feel consequence-free, leaving financial education to chance is no longer an option.

Research consistently shows that children are ready to absorb financial concepts far earlier than most parents think. According to a landmark study by the University of Cambridge, children form core money habits by age seven. That means the best time to start teaching kids about money is right now. This guide will walk you through why financial education matters, what core skills your child needs, how to teach those skills at every age, and the common pitfalls to avoid along the way.

Why Teaching Kids About Money Matters

When children grow up without a healthy understanding of money, the consequences often compound into something serious. Financial dependency, mounting debt, and poor self-esteem linked to money struggles are among the real outcomes for young adults who never received proper guidance.

On the flip side, children who learn financial skills early develop a sense of independence and confidence that extends well beyond their bank balance. According to the Consumer Financial Protection Bureau (CFPB), financial education in childhood leads to measurably better financial behaviors in adulthood.

Parents are the single greatest influence on how their children relate to money — stronger than school, friends, jobs, or media combined. That places a meaningful responsibility on every parent to be intentional about the lessons being passed on.

Core Money Skills Every Child Should Learn When Teaching Kids About Money

Regardless of age, there is a foundation of financial knowledge that every child should eventually build.

• Understanding the value of money — Children need to grasp that money represents effort and time before they can use it wisely.

• The difference between saving and spending — Children who understand this distinction from an early age make more thoughtful financial choices later.

• Basic budgeting — Even a simple division of money into jars labeled “save,” “spend,” and “give” is budgeting in its most honest form.

• Earning money — Whether through household chores, small tasks, or selling homemade crafts, the experience of earning money changes how a child values it.

• Giving and sharing — Generosity is woven into financial health. Children who grow up giving develop a healthier relationship with money.

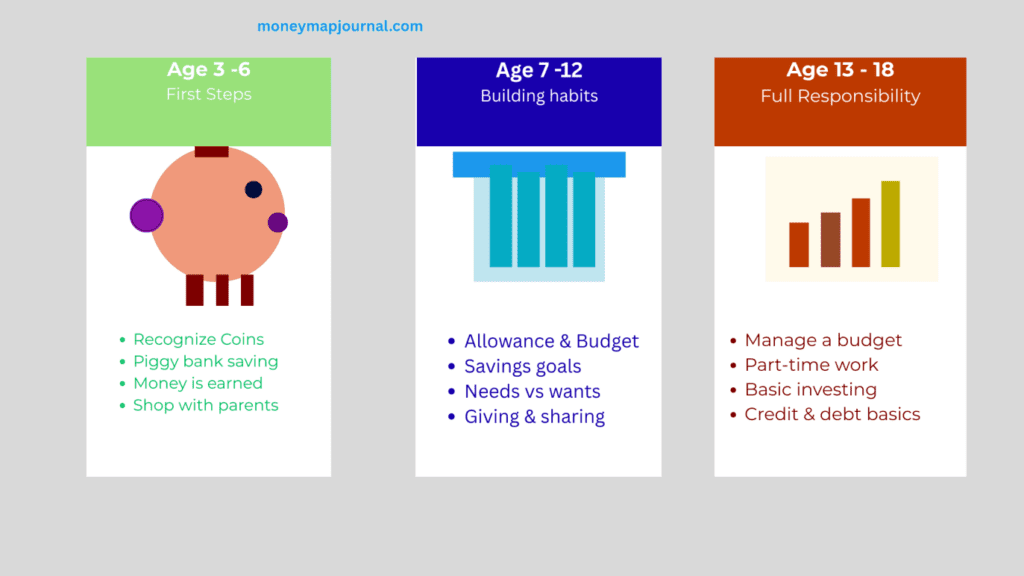

Teaching Kids About Money by Age

Teaching Kids About Money: Ages 3–6 (Introduction to Money)

At this stage, the goal is simple familiarity. Teaching kids about money starts here — with recognizing different coins and notes, understanding that they have different values, and learning that things cost money. Physical, tangible money is the best tool here.

A classic piggy bank is a child’s first savings account. Encourage your child to drop coins in regularly and watch the collection grow. The habit of setting something aside before spending is one of the most valuable behaviors you can introduce. For a full breakdown of how much to give at each age, see our guide: The Best Complete Kids Allowance Guide: How Much to Give at Every Age.

Teaching Kids About Money: Ages 7–12 (Building Money Habits)

This is the stage where teaching kids about money begins to produce real, lasting habits. Research cited by Investopedia confirms that consistent allowance paired with structured saving habits produces the most lasting results.

Introducing a regular allowance gives children hands-on practice managing their own money. Pair it with a simple system: a portion for spending, a portion for saving, and a portion for giving.

Encourage your child to set small savings goals. Walk them through how long it will take to save, help them track progress, and let them feel the genuine satisfaction of reaching that goal. Also consider using the best money apps for kids in 2026 to make tracking engaging and interactive.

Teaching Kids About Money: Ages 13–18 (Developing Financial Responsibility)

By the teenage years, teaching kids about money means removing the training wheels. Teenagers are capable of managing a real budget, understanding needs versus wants, and beginning to think about longer-term financial goals.

This is the right time to introduce how credit works, what debt actually costs, and how interest can either work for you or against you. A great framework to introduce at this stage is the 50/30/20 rule — allocating fifty percent of income to needs, thirty percent to wants, and twenty percent to savings. You can read more in our guide: The 50/30/20 Rule Explained: The Simplest Budgeting Method for Beginners.

Teenagers should also start thinking about their financial future. Starting a college fund early makes a real difference — our guide on How to Start a College Fund for Your Child walks through every step.

Practical Ways to Teach Kids About Money

Financial education is most powerful when it is experiential rather than theoretical. TTeaching kids about money is most effective through doing, not just talking. Doing money is transformative.

Take your children shopping and involve them in decisions — not just as observers but as active participants. Let them compare prices, choose between options, and understand why one product might be better value than another.

Role-playing buying and selling is a surprisingly effective tool, especially for younger children. Set up a pretend shop at home, use real or toy money, and let them practice being both the buyer and the seller.

Let your children make mistakes. If a child spends their entire week’s allowance on the first day and has nothing left by Friday, resist the urge to bail them out. That discomfort is the lesson. As Money.org notes, real financial learning comes from real consequences, not just classroom instruction.

Teaching Kids About Money Through Discipline

Discipline around money is not about deprivation — it is about intentionality. Teaching kids about money includes teaching them to delay gratification, which is one of the most reliable predictors of long-term financial wellbeing, according to research published by the American Psychological Association.

Encouraging your child to wait, to save, to plan, and to resist impulse spending builds a mental muscle that will serve them throughout their lives. Celebrate the moments when they show restraint. That positive reinforcement matters.

Establishing simple household rules around money also helps. Perhaps screen time purchases require a waiting period. Perhaps larger wants must be partly self-funded. Whatever the rules, consistency is what makes them effective.

Setting Financial Goals for Kids When Teaching Kids About Money

Goals give saving a purpose, and purpose makes discipline sustainable. Help your children distinguish between short-term goals and longer-term aspirations that require sustained effort over time.

Track progress visibly. A simple chart on the refrigerator, a savings thermometer they color in as they go, or a digital tracker on a family-friendly app all make abstract progress feel concrete and motivating.

The deeper lesson behind goal-setting is that money is a tool for achieving what you care about. That realization — that money is not an end in itself but a means to living intentionally — is one of the most important financial insights a person can have. For advanced wealth-building concepts to share with older teens, see: How to Create Multiple Streams of Income Starting With One Job.

Common Mistakes Parents Should Avoid When Teaching Kids About Money

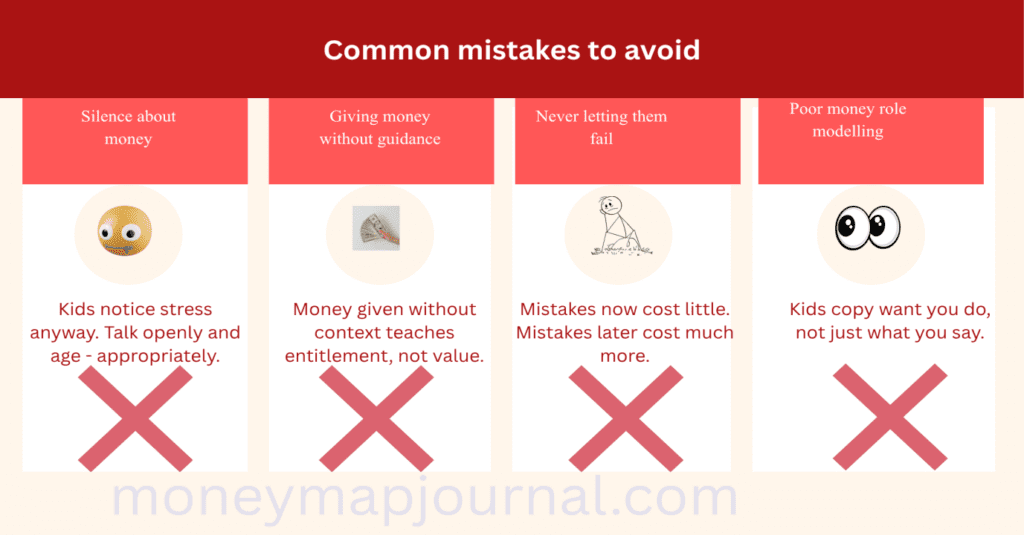

The most damaging thing a parent can do is say nothing. Treating money as a taboo subject does not protect children from financial stress — it simply leaves them without the tools to handle it.

Giving money without context or guidance is another common pitfall. Money handed over without expectation, explanation, or structure teaches children that money simply appears — which is not how the world works.

Being too controlling about money can also backfire. Children need latitude to make their own choices — including poor ones — within safe limits.

Perhaps most importantly: lead by example. Children observe constantly. They notice whether spending is impulsive or thoughtful, whether saving is talked about or actually practiced. Your financial behavior is their first and most lasting curriculum. This principle is echoed by the CFPB’s parent financial education resources.

Conclusion

Teaching kids about money is one of the most meaningful investments you will ever make — and unlike most investments, the returns are virtually guaranteed. Children who grow up financially literate are more independent, more resilient, and more equipped to build lives of genuine security and generosity.

You do not need to be a financial expert to do this well. You need to be willing to start, keep the conversation going, and make real-life practice a regular part of your family life.

The habits formed today — the piggy bank on the shelf, the savings goal on the chart, the moment your child hands over their own money and feels what it means to make a choice — those are the foundations of a financially confident adult.

Start small. Start now. The best way to begin teaching kids about money is with the lesson you give them today.