Roth IRA vs brokerage account — it’s one of the first real money decisions beginners face, and it’s more confusing than it needs to be. I still remember the afternoon I got my first “real” paycheck — the one that felt like actual money, not just cover-the-basics money. After rent, bills, and a completely unnecessary sneaker purchase, I had a few hundred dollars left over. I knew I should invest it. What I didn’t know was where.

Two browser tabs were open on my laptop: one explaining Roth IRAs, another walking through brokerage accounts. Both sounded smart. Both sounded complicated. I ended up closing both and putting the money in my checking account, where it sat idle for six months doing absolutely nothing. That’s the Roth IRA vs brokerage account dilemma in a nutshell.

If that sounds familiar, this post is for you. By the end of it, you’ll know exactly what each account is, how they’re different, and — most importantly — which one to open first.

Roth IRA vs Brokerage Account: Understanding Each Account

What Is a Roth IRA?

A Roth IRA is an individual retirement account funded with money you’ve already paid taxes on. That might sound like a disadvantage at first — no upfront tax break — but here’s the payoff: everything that grows inside a Roth IRA is completely tax-free. Dividends, capital gains, decades of compounding returns — none of it gets taxed when you withdraw it in retirement.

To take full advantage of those tax-free withdrawals, you need to meet two conditions: you must be at least 59½ years old, and your account must have been open for at least five years. Meet those two requirements, and you can pull out every dollar — including all the growth — without owing the IRS a single cent.

In the Roth IRA vs brokerage account debate, think of a Roth IRA like this: you pay full price for the seed today, but you never pay a cent on the harvest.

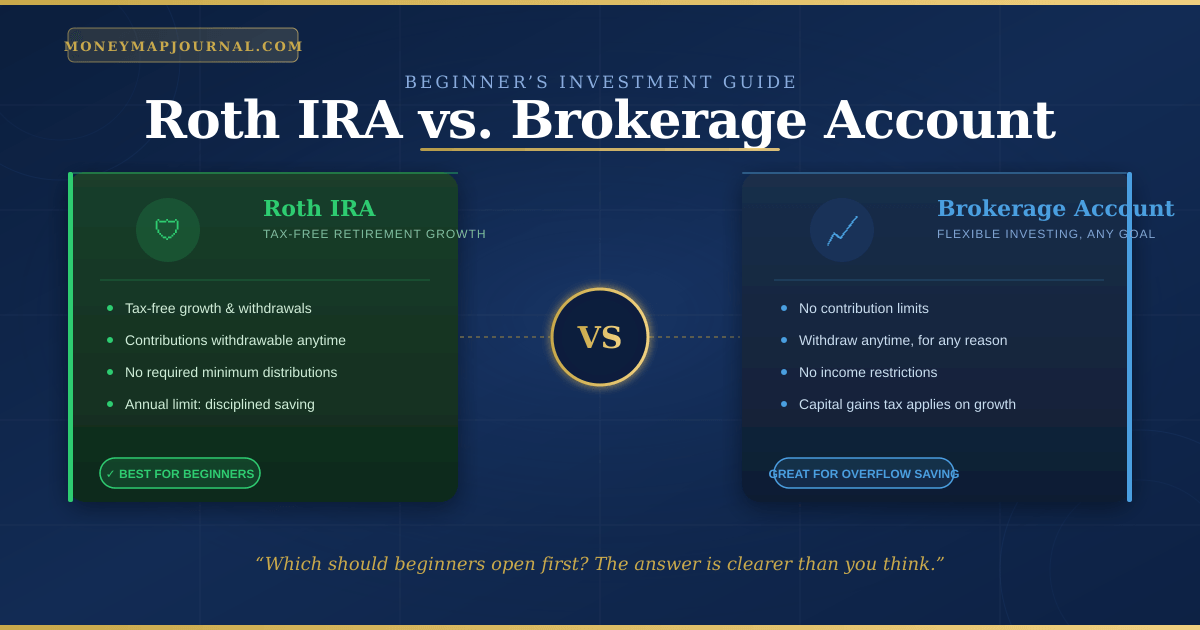

Key advantages of a Roth IRA:

- All investment growth inside the account is tax-free

- Qualified withdrawals in retirement are not taxed

- You can withdraw your original contributions at any time without penalty

- There are no required minimum distributions — you’re never forced to withdraw

- It’s available to anyone with earned income who falls within the income eligibility limits

- Annual contribution limits apply, keeping it a disciplined, structured savings vehicle

- It’s one of the most beginner-friendly retirement accounts available

What Is a Brokerage Account?

A taxable brokerage account is a standard investment account with no retirement label attached. You deposit money, buy investments — stocks, ETFs, mutual funds, bonds — and watch them grow. When you sell at a profit or receive dividends, the IRS comes knocking.

There’s no tax protection here. Short-term gains on assets held under a year are taxed at your ordinary income rate. Long-term gains on assets held over a year get better rates, but you’re still paying. Dividends and interest earned along the way are also taxable each year, whether you spend them or reinvest them.

What the brokerage account side of the Roth IRA vs brokerage account equation lacks in tax benefits, it makes up for in freedom. There are no contribution limits, no income restrictions, and no rules about when or why you can withdraw. You can invest as little or as much as you want. You can pull money out next week or in 30 years. It’s entirely your call.

Key advantages of a brokerage account:

- No contribution limits — invest as much as you want, whenever you want

- No income restrictions — available to everyone regardless of earnings

- Complete withdrawal flexibility — access your money anytime for any reason

- Wide range of investment options — stocks, bonds, ETFs, mutual funds, and more

- Great for medium-to-long-term goals that aren’t specifically tied to retirement

- Can be opened alongside any retirement account you already have

Roth IRA vs Brokerage Account: Side-by-Side Key Differences

Here’s where it gets simple. Once you see these two accounts compared directly, the choice for most beginners becomes obvious.

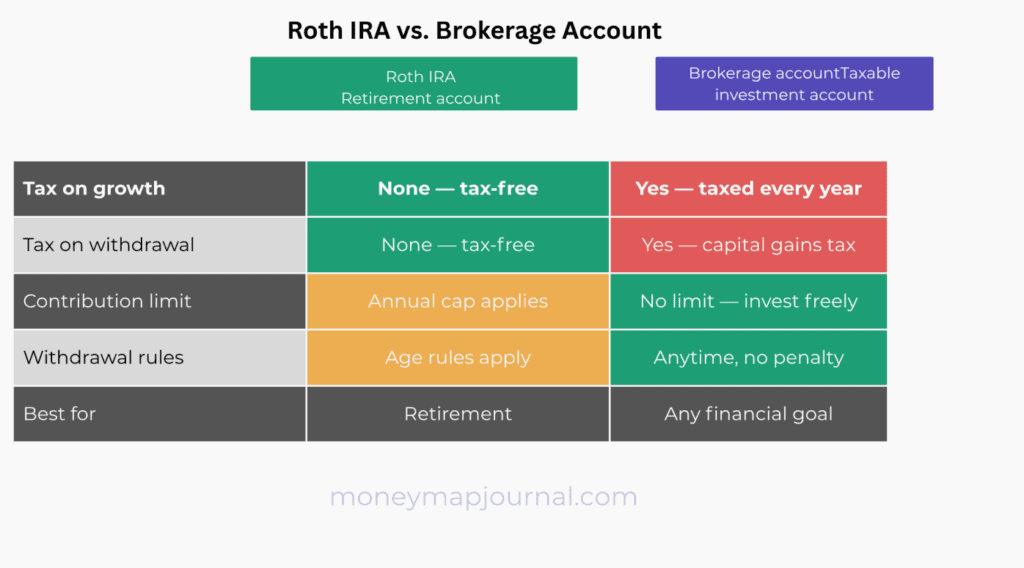

| Feature | Roth IRA | Brokerage Account |

| Tax on contributions | Paid upfront (after-tax) | Paid upfront (after-tax) |

| Tax on growth | None (tax-free) | Yes — capital gains + dividends taxed |

| Tax on withdrawals | None (if qualified) | Yes — capital gains tax applies |

| Annual contribution limit | Yes — capped each year | No limit |

| Income restrictions | Yes — eligibility phases out at higher incomes | None |

| Withdrawal flexibility | Contributions anytime; earnings have rules | Full flexibility, anytime |

| Early withdrawal penalty | Applies to earnings before age 59½ | None |

| Best suited for | Long-term retirement savings | Medium-term goals or overflow investing |

The biggest difference in the Roth IRA vs brokerage account comparison, in plain English: a Roth IRA protects your money from taxes for the rest of your life. A brokerage account gives you complete freedom but taxes you along the way.

Which Should Beginners Open First?

I won’t bury the lead. When it comes to the Roth IRA vs brokerage account decision, the majority of beginners — especially those in their 20s and 30s with a moderate income — should open the Roth IRA first. Here’s the case for it.

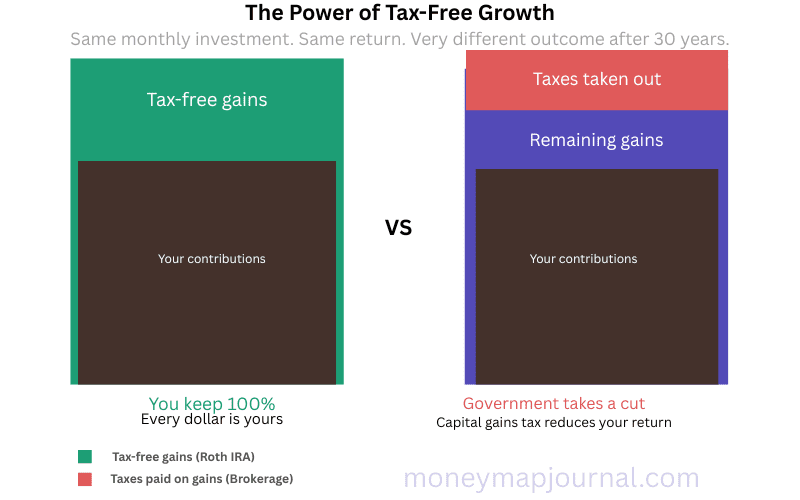

1. The Tax-Free Growth Is a Genuine Game-Changer

The most powerful thing about a Roth IRA isn’t what happens when you contribute — it’s what happens over the decades after. Your investments grow, year after year, and none of that growth is ever taxed.

In a Roth IRA vs brokerage account comparison, this is the key distinction: in a brokerage account, gains are taxed every time you sell, and dividends are taxed every year. Over a long investing timeline, that tax drag adds up to a significant difference in your final balance. The Roth eliminates it entirely.

2. You’re Likely in a Lower Tax Bracket Now Than You Will Be Later

The Roth IRA vs brokerage account timing advantage is real. The Roth IRA rewards people who pay taxes today rather than tomorrow — and for most beginners, today is the cheapest time to pay. Your early career years are often your lowest-earning years. As your career advances, your income rises, and so does your tax rate. By contributing to a Roth now, you lock in today’s lower tax rate and never pay taxes on that money again. That’s a trade worth making.

3. Your Contributions Stay Accessible

One of the biggest fears new investors have about retirement accounts is that the money gets locked away permanently. With a Roth IRA, your actual contributions — the dollars you put in — can be withdrawn at any time, for any reason, without taxes or penalties. Only the earnings are subject to the age and time restrictions.

This makes the Roth IRA far more beginner-friendly than most people realize in the Roth IRA vs brokerage account choice. Yes, it’s primarily a retirement account and you should treat it that way, but knowing you can access your contributions if life throws you a curveball removes a huge psychological barrier to getting started.

4. It Builds a Powerful Savings Habit

The annual contribution limit on a Roth IRA might seem like a restriction, but for beginners it’s actually a gift. It gives you a clear, achievable savings target each year — a finish line you can actually reach. The discipline of consistently funding your Roth IRA year after year is one of the most effective financial habits you can build, and the structure of the account helps enforce it.

5. Time Is Your Biggest Asset — and the Roth Rewards It Most

Compound growth needs time to work. The earlier you start contributing to a Roth IRA, the longer your money has to grow tax-free, and the more dramatic the results become. A young investor who starts early and contributes consistently will almost always end up with significantly more than someone who starts later, even if that later investor contributes larger amounts. With a Roth IRA, every extra year of growth is a year the government doesn’t get to tax.

When a Brokerage Account Makes More Sense

To be fair to the brokerage account side of the Roth IRA vs brokerage account debate, there are situations where it either replaces or supplements the Roth IRA.

Your income exceeds the Roth IRA eligibility limits. Roth IRAs have income thresholds, and once your earnings rise above a certain point, you become ineligible to contribute directly. If that’s your situation, a taxable brokerage account becomes your primary vehicle for additional savings. (A strategy called the “backdoor Roth” is worth exploring with a financial advisor if you’re in this position.)

You’ve already maxed out your retirement accounts. If you’re contributing the maximum allowed to your employer retirement plan AND your Roth IRA, well done — seriously. The next step is opening a brokerage account for the overflow. The tax-advantaged buckets are full; keep building wealth in the open market.

You’re saving for a goal five to ten years away. Planning to buy a home in seven years? Saving toward a business launch or a major life expense? These goals sit in a middle ground — too far out for a savings account, but too near for a strictly retirement-focused account. A brokerage account is ideal here. You can invest in low-cost index funds, let the money grow, and access it whenever you’re ready, with no restrictions.

The Beginner’s Order of Operations

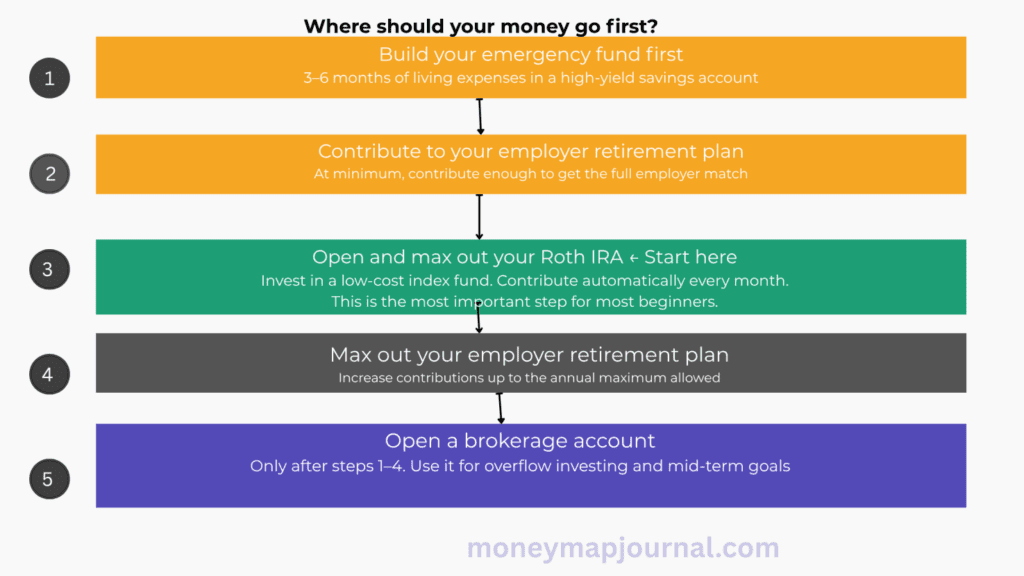

If you’re just starting out and feeling overwhelmed by the Roth IRA vs brokerage account decision, here is the sequence I’d recommend following — in order:

Step 1 — Build your emergency fund. Before you invest a single dollar, save three to six months of living expenses in a high-yield savings account. This is your financial cushion. Without it, any unexpected expense or market dip could force you to sell investments at the worst possible time.

Step 2 — Contribute to your employer retirement plan. If your employer offers a workplace retirement plan with a contribution match, contribute enough to claim every dollar of that match. Employer matching is essentially free money added directly to your retirement savings — take full advantage of it before anything else.

Step 3 — Open and fund your Roth IRA. This is the step most beginners skip — and it’s the most important one. Open a Roth IRA, contribute regularly up to the annual limit, and invest it in a simple, low-cost index fund. Set up automatic monthly contributions if you can. This is where long-term wealth is quietly built.

Step 4 — Maximize your employer retirement plan. Once the Roth IRA is funded, direct any remaining investment dollars back into your workplace retirement plan, working toward the annual maximum contribution.

Step 5 — Open a brokerage account. Only after steps 1 through 4 are covered does the brokerage account side of the Roth IRA vs brokerage account equation enter the picture. At that point, it becomes a powerful tool for building additional wealth with complete flexibility — whether for medium-term goals or further long-term growth.

The truth is, most beginners will build an incredibly strong financial foundation just by nailing steps 1 through 3. Steps 4 and 5 can come later as your income and savings rate grow.

You Don’t Have to Choose Just One Forever

Here’s the bigger picture: the Roth IRA vs brokerage account question isn’t about picking one forever. The goal is to build a layered investment strategy over time — a Roth IRA for tax-free retirement wealth, a workplace retirement plan for tax-advantaged growth at scale, and eventually a brokerage account for flexible mid-term and long-term goals.

The most financially secure people aren’t relying on a single account. They’ve built a system where every dollar has a job, and each account type plays a specific role. The Roth IRA vs brokerage account question isn’t really an either/or — you build that system one account at a time, and for almost every beginner, the Roth IRA is the right place to start.

Final Verdict: Open the Roth IRA First

Open it today. Not next month. Not after you “figure out” your finances. Today.

The biggest advantage you have right now is time. Compound growth needs years to work its magic, and every year you delay is a year of tax-free growth you can never get back. You don’t need to understand everything about investing to get started. You just need to open the account, contribute what you can afford, and put it in a simple index fund. That’s it.

The worst financial decision I ever made was closing those browser tabs and doing nothing. If you’re still weighing the Roth IRA vs brokerage account choice — you’re already ahead of where I was. You read the whole thing. Now go take the next step.

Related reading: Investing for Beginners: What to Do With Your First $1,000 — MoneyMapJournal

Also see: The 7 Habits of People Who Build Wealth From Scratch — MoneyMapJournal