Published on moneymapjournal.com · Personal Finance · 10 min read

Let me ask you something. If someone asked you right now, “What is your net worth?” — would you know the answer? If you hesitated, you are not alone. Most people track their income or their monthly budget, but very few actually sit down and calculate their net worth. And that, my friend, is one of the biggest blind spots in personal finance.

I started tracking my own net worth a few years ago, and it completely changed the way I see money. It was not about how much I was earning — it was about what I was keeping and growing. That single shift in perspective made me more intentional, more strategic, and honestly, more motivated to keep going.

In this article, I am going to walk you through what net worth means, how to calculate it accurately, why it matters — and most importantly — practical, proven ways to grow it every single year. Whether you are just starting out or already on your financial journey, this one is for you.

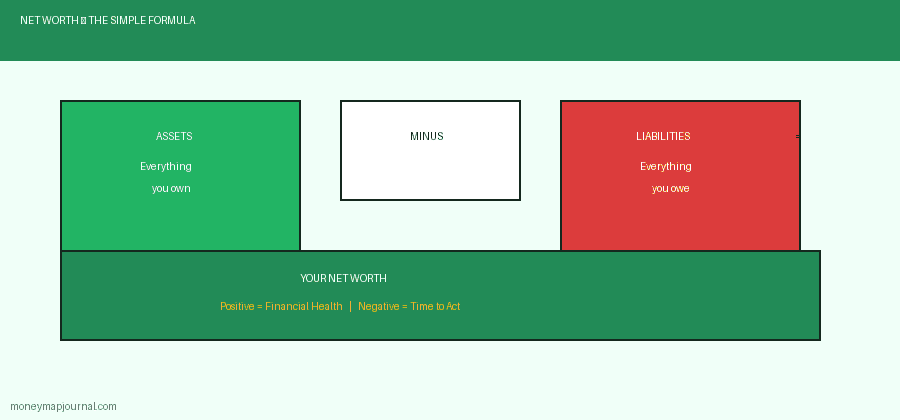

💡 Quick definition: Net worth = Total Assets − Total Liabilities. It is the single most honest number in your financial life.

What Is Net Worth? (And Why It Matters More Than Your Salary)

Your salary tells you how much money is flowing in. Your net worth tells you how much is actually staying. Net worth is the total value of everything you own — your assets — minus everything you owe — your liabilities. It is a snapshot of your real financial health at any given moment.

Think about it this way: someone earning a huge salary but spending everything and carrying heavy debt could actually have a lower net worth than someone on a modest income who saves consistently, invests wisely, and avoids unnecessary debt. Income is just one part of the picture. Net worth is the full story.

Lenders, investors, and financial institutions look at net worth to assess your financial stability. It also determines your eligibility for certain types of investments and loans. More practically, it gives you a benchmark — a number to beat every year.

The Net Worth Formula | moneymapjournal.com

How to Calculate Your Net Worth (Step by Step)

The formula is beautifully simple:

Net Worth = Assets − Liabilities

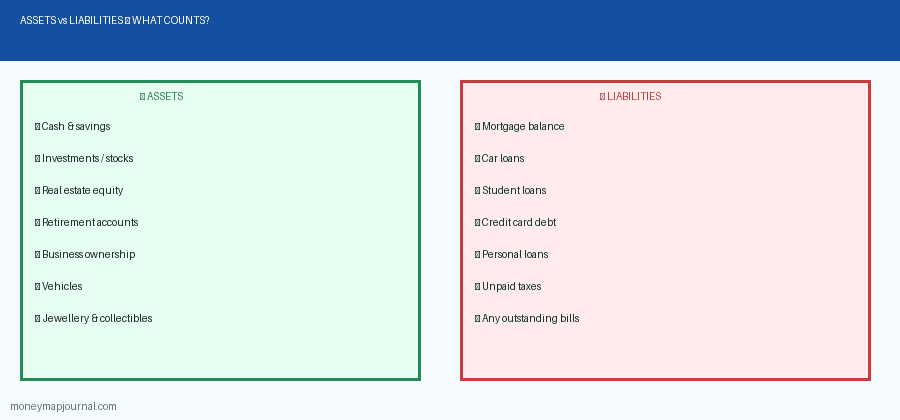

Step 1 — List All Your Assets

An asset is anything you own that has financial value. Be thorough but realistic. Here is what to include:

- Cash and savings: all balances across checking, savings, and money-market accounts.

- Investments: stocks, bonds, unit trusts, mutual funds, ETFs, crypto holdings.

- Retirement accounts: pension plans, 401(k), IRA, provident funds, and any workplace or government retirement schemes.

- Real estate equity: the current market value of property you own, minus any outstanding mortgage.

- Business ownership: your equity stake in any business you own or co-own.

- Vehicles: current resale value of your car, motorbike, or other vehicles.

- Other valuables: jewellery, artwork, collectibles, and other items with significant cash value.

Step 2 — List All Your Liabilities

A liability is any debt or financial obligation you owe to others. Be honest — leaving things out only hurts you:

- Outstanding mortgage balance on any property.

- Car loans and hire purchase agreements.

- Student loans or any government education debt.

- Credit card balances (every card, every cent).

- Personal loans from banks, SACCOs, or individuals.

- Unpaid taxes or government levies.

- Any other debt you are legally obligated to repay.

Step 3 — Do the Math

Subtract total liabilities from total assets. If the result is positive, congratulations — your assets outweigh your debts. If it is negative, do not panic. It is common early in life, especially with student loans or mortgages. The important thing is to track it and move it in the right direction.

Need a real-life example of building from zero? Read our guide on how to save money on a tight budget’, which is a great starting point if your net worth is currently negative.

Assets vs Liabilities — What to Include | moneymapjournal.com

Positive vs Negative Net Worth — What Does It Mean for You?

Positive net worth means your assets exceed your liabilities. This is the goal. A positive and growing net worth signals that you are making smart financial decisions — saving, investing, and managing debt well.

Negative net worth means your debts outweigh what you own. This can feel discouraging, but it is not a life sentence. Many people start with negative net worth — especially students, young professionals, or those who have faced unexpected financial hardship — and go on to build significant wealth.

📌 Real talk: A negative net worth is not a failure. It is a starting point. What matters is the direction you are moving.

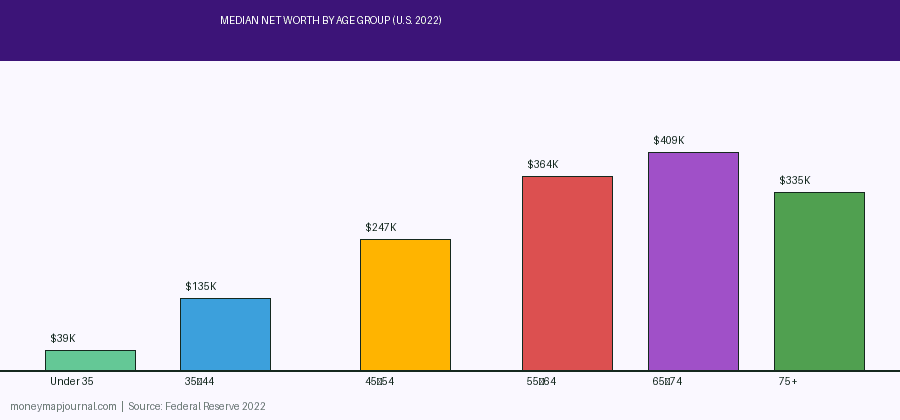

- Under 35: median net worth of about $39,000

- Ages 35–44: approximately $135,600

- Ages 45–54: approximately $247,200

- Ages 55–64: approximately $364,500

- Ages 65–74: approximately $409,900

These numbers are useful as benchmarks, but remember — your personal context, currency, and country matter enormously. Wherever you are in the world, the principles remain exactly the same: grow assets, shrink liabilities, and track progress.

Median Net Worth by Age Group (U.S. 2022) | moneymapjournal.com

5 Proven Strategies to Grow Your Net Worth Every Year

Here is where things get exciting. Growing your net worth is not about luck or a massive windfall. It is about consistent, intentional action — year after year. Here are the five strategies I personally believe in and practice:

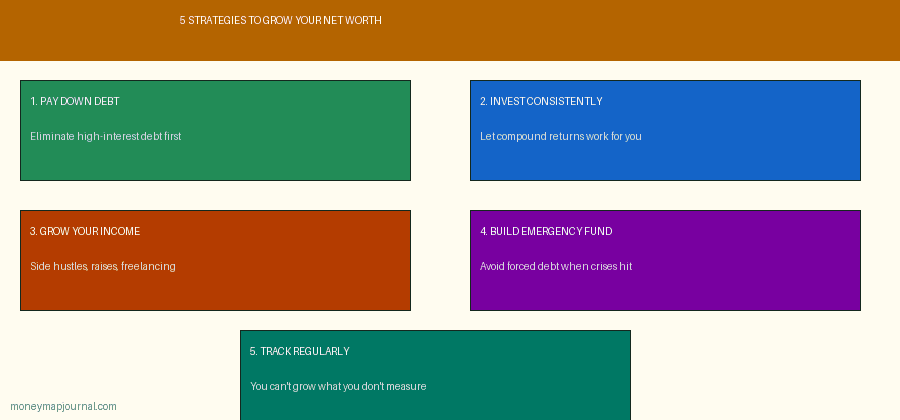

1. Pay Down Debt Aggressively

Every unit of currency you eliminate from your debt column directly increases your net worth. Start with high-interest debt first (the debt avalanche method) or tackle the smallest balance first for a psychological win (the debt snowball method). Either way, debt reduction is one of the fastest paths to net worth growth. Learn more about budgeting strategies on Investopedia.

2. Invest Consistently (Let Compound Interest Do the Heavy Lifting)

Saving alone is not enough. Money sitting idle in a low-interest account loses value to inflation over time. Investing allows your money to work for you through the power of compound returns — where your investment earnings generate their own earnings. Whether you invest in the stock market, index funds, or real estate, the earlier you start, the better. I have written about ETFs vs Mutual Funds and index funds for beginners right here on Money Map Journal — do check those out.

3. Grow Your Income

More income means more capital to invest and pay off debt. Consider negotiating a raise (our salary negotiation guide can help), starting a side hustle, or building passive income streams. The goal is not just to earn more — it is to keep more of what you earn and redirect it toward assets.

4. Build and Protect Your Emergency Fund

Nothing derails net worth growth faster than an emergency that forces you into debt. A well-funded emergency fund — ideally three to six months of living expenses — acts as a financial buffer. It protects the progress you have already made. Read our detailed piece on emergency funds and why you need one.

5. Track Your Net Worth Regularly

This one sounds obvious, but it is deeply underestimated. You cannot grow what you do not measure. I recommend calculating your net worth at least once a year — and quarterly if you are in an active growth phase. Use a spreadsheet, an app like Personal Capital, or a simple notebook. What matters is consistency.

5 Strategies to Grow Your Net Worth | moneymapjournal.com

Common Mistakes That Shrink Your Net Worth (Avoid These!)

I have seen these mistakes over and over again — including in my own financial life early on:

- Lifestyle inflation: earning more but spending even more, so net worth stays flat or falls.

- Ignoring debt: minimum payments feel manageable until compound interest snowballs.

- Not investing: saving is great, but idle cash does not grow your net worth meaningfully.

- Over-leveraging on depreciating assets: taking loans to buy things that lose value (like luxury cars) increases liabilities without adding lasting asset value.

- Skipping the audit: not reviewing your finances regularly means you miss both problems and opportunities.

Net Worth Is Universal — It Works Wherever You Are

The net worth principles in this article are universal — they apply regardless of where you live or what currency you use. The specific assets and liabilities may look different from country to country (land ownership laws, pension schemes, tax structures, real estate markets), but the formula and the philosophy are the same. Calculate. Track. Grow.

No matter where you are on the income spectrum or which part of the world you call home, the path to building net worth is the same: be intentional about your assets, stay on top of your liabilities, and let time and compounding work in your favour. Resources like Fidelity’s personal finance guides are an excellent external reference, even if they are U.S.-focused, because the principles translate globally.

Final Thoughts — Your Net Worth Journey Starts Today

Here is what I want you to take away from this article: your net worth is not a fixed number. It is a living, breathing reflection of the financial decisions you make every single day. It can grow — and it will grow — if you commit to the right habits.

You do not need a six-figure salary to build impressive net worth. You need clarity, consistency, and courage. The courage to face your numbers honestly, to resist the pressure to keep up with others, and to play your own long game.

So here is your action step for today: grab a piece of paper (or open a spreadsheet), list every asset and every liability, do the calculation, and write down your baseline net worth. Then set a goal for where you want it to be 12 months from now. That number is your financial north star.

🌟 “Someone is sitting in the shade today because someone planted a tree a long time ago.” — Warren Buffett. Your financial future is being planted right now, with every decision you make.

I am rooting for you. Keep going — one step, one decision, one year at a time. And if you found this article helpful, share it with someone who needs to hear it today. Let us grow together right here at Money Map Journal.