Most people don’t fail at saving money because they’re bad with money. They fail because nobody ever showed them a system for managing a monthly budget.

I learned this the hard way. After months of job hunting, the call I had been waiting for finally came — an interview, then an offer, then my first real salary landing in my account. I was excited. For the first time, money was coming in consistently. But eight months later, I had almost nothing to show for it. The bills were paid, but I wasn’t moving forward. Every time I set money aside, something would come up and wipe it out. I felt completely stuck.

Then one evening, scrolling through TikTok, I came across something called a monthly budget. It sounded simple enough — but when I went looking for one that actually made sense for my life, I couldn’t find it. So I built my own.

That decision changed everything. Using a zero-based budgeting method — where every dollar of your income gets assigned a job before the month begins — I went from saving nothing to consistently saving 15% of my salary every single month. Was it easy at first? No. I had to cut back on things I had grown comfortable spending on. But within a few months, I had more financial progress than I had made in the previous eight months combined.

If you are starting your first job, trying to stop living paycheck to paycheck, or simply tired of watching your money disappear without knowing where it went, this guide is for you. I am going to walk you through exactly how to build a monthly budget using the zero-based method, step by step, with a free Google Sheets template you can start using today.

What Is Zero-Based Budgeting?

Zero-based budgeting is a method where you assign every single dollar of your income a specific job before the month begins — so that when you subtract all your expenses, savings, and goals from your income, you are left with exactly zero.

Zero does not mean you have no money left. It means every dollar has been accounted for. Nothing is floating around waiting to be spent on something you did not plan for.

Here is the simplest way to think about it:

Income − Expenses − Savings − Goals = 0

For example, if you earn $3,000 a month, you assign all $3,000 across your rent, groceries, transport, savings, and any financial goals — until nothing is unassigned. Every dollar has a destination before the month even starts.

This is different from how most people budget — or try to. Most people spend first and save whatever is left over. The problem is that nothing is ever left over. Zero-based budgeting flips that completely. You decide where your money goes instead of wondering where it went.

The term was originally developed as a corporate financial planning tool. Still, it was popularised for personal finance by financial author Dave Ramsey, whose EveryDollar app is built entirely around this method. Today, it is one of the most recommended budgeting systems for beginners because it works on any income, high or low.

How Does Zero-Based Budgeting Work?

Zero-based budgeting works by giving every dollar of your income a specific category before the month starts. Unlike traditional budgeting, where you track spending after it happens, zero-based budgeting is proactive — you make decisions about your money before the month begins, not after it is already gone.

The process has three core stages:

Stage 1 — Know Your Income. Before you can assign anything, you need one clear number: exactly how much money is coming in this month. For salaried employees, this is straightforward — it is your take-home pay after tax. If you have a side hustle or irregular income, use your lowest expected month as your baseline. It is always better to budget conservatively and have money left over than to over-budget and fall short.

Stage 2 — List Every Expense. Write down everything your money needs to cover this month. This includes fixed expenses that never change — rent, loan repayments, subscriptions — and variable expenses that fluctuate, like groceries, fuel, and entertainment. Most people are genuinely surprised at this stage. Seeing everything written down in one place is often the first honest conversation someone has with their money.

Stage 3 — Assign and Adjust Until You Hit Zero. Now you match your expenses against your income. Keep adjusting categories until your income minus all expenses, savings, and goals equals zero. If you have money left over, give it a job — move it into savings, an emergency fund, or a financial goal. If you are over budget, trim categories until the numbers balance.

The entire power of this method is in that final zero. It removes the grey area where money disappears.

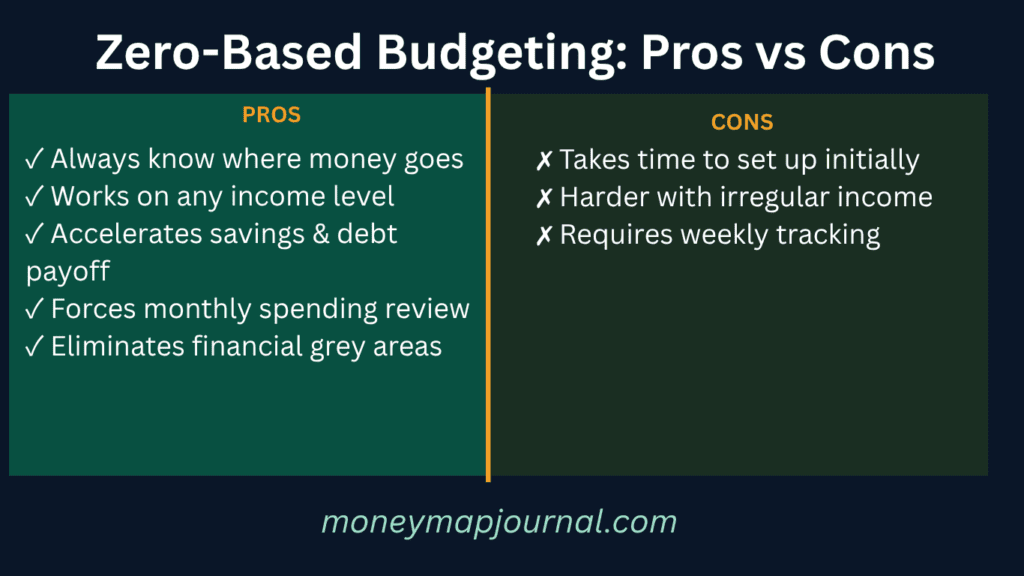

Zero-Based Budgeting Advantages and Disadvantages

No budgeting method is perfect for every person. Here is an honest look at what makes zero-based budgeting powerful — and where it can feel challenging, especially when you are just starting.

Advantages

You always know where your money is going. There are no surprises at the end of the month. Every dollar was assigned a purpose on day one, so overspending in one area is visible immediately.

It works on any income level. Whether you earn a lot or a little, the math is the same. You are working with what you have, not what you wish you had. This is what made it work for me — I was not earning a large salary, but zero-based budgeting made my income feel intentional for the first time.

It accelerates savings and debt repayment. Because you are assigning money to savings before you spend on anything else, saving stops being an afterthought. It becomes a fixed expense just like your rent.

It forces you to review your spending every month. Most people set a budget once and forget it. Zero-based budgeting requires you to rebuild it every month. That regular check-in keeps you honest and catches problems early.

It eliminates financial grey areas. That vague “miscellaneous” category where money quietly disappears? Zero-based budgeting forces you to name it. If you cannot name where it is going, it should not be going there.

Disadvantages

It takes time, especially in the beginning. Your first zero-based budget will take longer than you expect. Setting up your categories, finding your real numbers, and balancing the equation to zero can take an hour or two the first time. It gets faster — by month three, you will do it in under 20 minutes — but the initial setup requires patience.

Variable income makes it harder. If your income changes month to month, building a zero-based budget requires more discipline. You have to budget from your lowest expected income and rebuild the plan when more comes in.

It requires honest tracking throughout the month. The budget only works if you check it regularly. Creating it and forgetting it defeats the purpose entirely. You need to track your actual spending against your plan at least once a week.

Is it worth it despite the downsides? For most beginners — yes. The disadvantages are mostly about effort and habits, not about the method itself. The effort decreases significantly after the first two months.

How to Create a Zero-Based Monthly Budget Step by Step

This is the section you came here for. Follow these five steps exactly, and you will have a working zero-based budget by the time you finish reading.

Step 1 — Write Down Your Total Monthly Income

Start with your net income — the amount that actually arrives in your account after tax and any deductions. Do not use your gross salary. If you have multiple income sources, add them all together.

Example: Monthly take-home salary — $2,400. Freelance side income — $200. Total monthly income — $2,600.

If your income varies, use the lowest amount you reliably receive. You can always adjust upward — you cannot adjust a budget built on income that did not arrive.

Step 2 — List Every Single Expense

Write down every category your money goes to this month. Split them into two groups:

Fixed expenses — amounts that do not change month to month: Rent or mortgage, loan repayments, insurance premiums, subscriptions (Netflix, Spotify, gym membership), internet, phone bill.

Variable expenses — amounts that change each month: Groceries, fuel or transport, electricity, water, clothing, entertainment, personal care, dining out.

Do not skip anything. Even small subscriptions add up. This step is where most people discover they have been spending money on things they forgot they were paying for.

Step 3 — Assign Every Dollar a Category

Now subtract your expenses from your income one category at a time. Be specific — “food” is not a category. “Groceries — $300” is a category.

Keep going until every dollar of your income has been assigned somewhere. Your savings, emergency fund contribution, and any financial goals are categories, too — assign them just like rent. Savings is not what is left over. Savings is a line item.

Step 4 — Balance Until You Reach Zero

Subtract everything from your income. If you have money left over, assign it — add it to savings, an extra debt payment, or a goal fund. If you are over budget, you need to trim. Go through your variable expenses first — these are where adjustments are easiest to make.

The goal is:

Total Income − Total Assigned = $0

This step is where the hard conversations happen. It was at this step that I realised I was spending more on things I did not actually value than on things that mattered to me. The budget makes that visible. That visibility is uncomfortable and useful in equal measure.

Step 5 — Track and Adjust Every Week

A budget is not a document you create once and file away. Check it every week. Compare what you planned to spend against what you actually spent. If groceries run out, something else needs to come down. If you underspent on fuel, move that surplus to savings.

By the end of the month, you will have a much more accurate picture of your real spending habits — and your month two budget will be better than month one because of it.

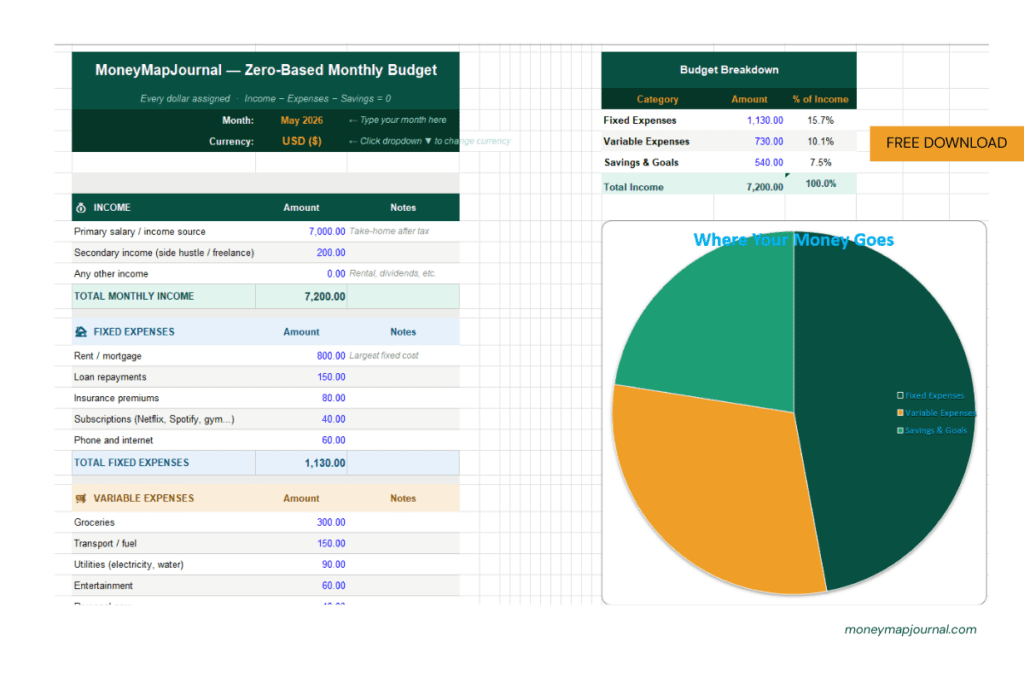

Free Monthly Budget Template (Google Sheets)

How Much Should You Budget Monthly for Key Expenses?

One of the most common questions beginners ask when building their first budget is: Am I spending the right amount on this? There is no single perfect answer because your income, location, and life situation are unique to you. However, there are widely used percentage guidelines that give you a reliable starting point.

The most practical framework for a zero-based budget is the 50/30/20 rule as a starting reference — but adjusted to fit your real life:

| Category | Suggested % of Income | Example on $2,600/month |

|---|---|---|

| Housing (rent/mortgage) | 25–30% | $650 – $780 |

| Food & Groceries | 10–15% | $260 – $390 |

| Transport & Fuel | 10–15% | $260 – $390 |

| Utilities & Bills | 5–10% | $130 – $260 |

| Personal Care | 3–5% | $78 – $130 |

| Entertainment & Dining | 5–10% | $130 – $260 |

| Savings & Emergency Fund | 15–20% | $390 – $520 |

| Debt Repayment | 5–10% | $130 – $260 |

| Financial Goals | 5–10% | $130 – $260 |

How Much Should You Budget for Specific Expenses?

Groceries: A reasonable grocery budget for a single person is $150–$300 per month, depending on your city and eating habits. For a family of four, $400–$700 is a realistic range. The key is to plan your meals before you shop — impulse buying at the grocery store is one of the fastest ways to blow a monthly budget.

Transport and Car Maintenance: If you own a car, budget not just for fuel but for maintenance. A reliable rule is to set aside $50–$100 per month specifically for car maintenance — oil changes, tyres, unexpected repairs. Most people ignore this until something breaks, then wonder where the money will come from. Your monthly budget should answer that question before the problem arrives.

Housing: Financial experts widely recommend keeping housing costs below 30% of your take-home income. If your rent is above that threshold, that is your signal to either increase your income or find ways to reduce costs elsewhere in your monthly budget. Housing is usually your largest fixed expense and the hardest to reduce quickly — which is exactly why it should be the first category you fill in.

Utilities: Budget slightly higher than your average utility bill to cover seasonal spikes. If your electricity averages $80 a month but runs $120 in summer, budget $100 as your baseline and let the surplus roll into next month’s category.

Savings: This is the number I want you to pay closest attention to. When I started budgeting, I was saving 0% of my income. After building my monthly budget, I was saving 15% consistently. Save at a minimum of 10–20% of your income every single month, even if you have to start at 5% and build up. The habit matters more than the amount in the beginning.

The most important thing this table tells you is this: no category should be invisible. Every area of your spending deserves a number, a limit, and your attention.

Best Free Apps for Zero-Based Budgeting

Once you understand the method, the right app makes it significantly easier to stick to your monthly budget throughout the month. You do not need a paid app to get started — these free options cover everything a beginner needs.

1. EveryDollar (Free Tier) Built specifically for zero-based budgeting by Dave Ramsey’s team. The free version lets you create a monthly budget manually, assign every dollar to a category, and track your spending as the month progresses.

2. Goodbudget (Free Tier) Goodbudget uses a digital version of the envelope budgeting method, which pairs naturally with zero-based budgeting. You create virtual envelopes for each spending category and fill them with your budgeted amounts at the start of the month.

3. Google Sheets (Free — Always) Never underestimate a well-built spreadsheet. The free budget template included in this article is built in Google Sheets, works on any device, and can be customised to fit your exact monthly budget categories.

4. Money Manager (Free Tier — Mobile) A clean mobile app for tracking daily expenses against your monthly budget. You enter each transaction as it happens, which keeps your budget accurate in real time.

5. Your Bank’s Built-In App. Before downloading anything, check whether your bank already offers budgeting tools inside its app. Many modern banks now include spending category breakdowns and monthly summaries. Using what you already have is always the most frictionless starting point.syncing, but the free tier is more than enough to start. Best for: Beginners who want a dedicated zero-based budgeting app.

A Note on Paid Apps: YNAB (You Need A Budget) is widely considered the gold standard for zero-based budgeting apps and comes up frequently in searches. It is excellent — but it costs $14.99 per month after a free trial. As a beginner budgeter, start with the free options above. Once your budget is consistently working and your income has grown, revisit YNAB as an upgrade.

Frequently Asked Questions

What does zero-based budgeting require? Zero-based budgeting requires three things: your total monthly income, a complete list of your expenses, and the discipline to assign every dollar before the month begins. A simple spreadsheet or free app is all the technology required to build your monthly budget.

Is zero-based budgeting good for beginners? Yes — and in many ways it is better for beginners than for experienced budgeters. When you are new to managing money, zero-based budgeting forces you to learn exactly where your money is going from day one. The first monthly budget is the hardest. By month three, it becomes second nature.

What is the difference between zero-based budgeting and the 50/30/20 rule? The 50/30/20 rule divides your income into three broad buckets. Zero-based budgeting assigns a specific amount to every individual category in your monthly budget, which means you have a much clearer picture of exactly where each dollar is going.

Can I use zero-based budgeting with an irregular income? Yes. The key adjustment is to build your monthly budget from your lowest expected income. Cover your essential fixed expenses and savings first. When a higher-income month arrives, assign the extra money immediately.

How do I handle unexpected expenses in a zero-based budget? This is exactly what your emergency fund category in your monthly budget is for. From your very first budget, assign a fixed amount every month to an emergency fund — even if it is only $50.

What if I go over budget in one category? Adjust another category in your monthly budget downward by the same amount. The budget must always balance. Going over occasionally is normal, especially in your first few months.

Conclusion

Zero-based budgeting will not solve every financial problem overnight. What it will do is give you clarity about where your money is actually going and what is possible when every dollar in your monthly budget has a purpose.

I started this journey eight months into my first job with almost nothing saved. Building a monthly budget was uncomfortable at first. But within a few months, I was saving 15% of my salary consistently — not because my income had changed, but because my decisions had.

You do not need to earn more money to start. You need a plan for the money you already have.

Start with Step 1 today. Write down your income. Write down your expenses. Assign every dollar a job. Download the free zero-based budget template below, make a copy in Google Sheets, and fill in your numbers today.

And if you found this guide useful, join the MoneyMap Journal email list below. Every week, I share one practical money tip to help you budget smarter, save more, and build wealth from wherever you are starting.