Picture this: your car breaks down on a Monday morning. Your employer calls with unexpected news on a Wednesday. Your child needs hospital care on a Friday evening. None of these events ask for permission. They just happen.

If any of those scenarios made your stomach drop a little, you are not alone. Most people go through life without a proper emergency fund in place, and when something hits, they are left scrambling for credit cards, loans, or money borrowed from family.

I strongly believe that having an emergency fund in place is crucial. The point is that people face emergencies all the time, and it is essential to be prepared. A hospital visit, unemployment, repairs, and any other type of expenses linked to an unforeseen situation can really harm your budget. Having money saved exclusively for emergencies gives you a sense of safety and allows you to avoid numerous complications tied to money-related problems.

This guide will answer the two questions that matter most: how much you really need, and where the best place to keep it is. By the time you finish reading, you will have a clear, practical plan you can start on today.

Before you read on: If you are still working on your budget foundation, start with our guide on How to Build a Monthly Budget That Actually Works. Your emergency fund sits inside your budget, and the two go hand in hand.

What Is an Emergency Fund?

An emergency fund is money you set aside exclusively for unexpected financial situations. It is not your spending money. It is not your investment portfolio. It is not your holiday savings. It is a dedicated financial buffer that exists for one purpose only: to protect you when life does not go to plan.

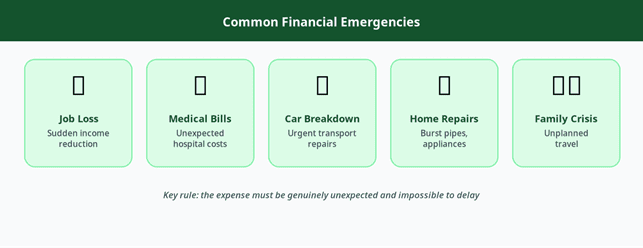

Common emergencies that qualify include:

- Sudden job loss or reduction in income

- Unexpected medical or hospital bills

- Urgent home repairs such as a burst pipe or broken appliance

- Car breakdowns or urgent transport costs

- Unplanned travel for a family crisis

The key word is unexpected. A holiday is not an emergency. A new phone is not an emergency. Your emergency fund should never be withdrawn for anything that could have been planned for or saved toward separately.

It is also worth being clear about what an emergency fund is not. It is not a savings account for goals. It is not an investment. And it is not extra money that sits there until you want something. It is a boundary you draw around a specific amount of money and protect no matter what.

The five most common financial emergencies that justify drawing from your emergency fund. Anything that could have been planned for or saved toward separately does not qualify.

Why an Emergency Fund Matters More Than You Think

Most people understand that saving for emergencies is a good idea. But understanding it and actually doing it are two very different things.

Here is what happens without one: you face an unexpected cost, you have no buffer, so you reach for a credit card or take out a loan. Now you have the original problem plus a debt with interest. That debt eats into your next month’s budget. You have less breathing room. The next small surprise hits harder than it should. This is how people end up stuck.

An emergency fund breaks that cycle. It means a broken-down car stays a frustrating inconvenience rather than a financial crisis. It means a hospital bill gets paid without wiping out your rent money. It means you can face job uncertainty without panic.

The peace of mind that comes with having an emergency fund is not a small thing. It changes how you make decisions. It changes how you sleep at night. And it changes how quickly you can move forward financially because you are not constantly starting over.

According to Vanguard, having even a modest emergency buffer can be as powerful as having significantly larger assets, because it gives you immediate financial resilience when you actually need it most. This view is reinforced by research from the Consumer Financial Protection Bureau (CFPB), which notes that people with emergency savings are significantly less likely to turn to high-cost debt when a financial shock hits.

How Much Money Should You Have in an Emergency Fund?

This is the question most people get wrong because they look for a single number that fits everyone. The reality is that the right amount of money in your emergency fund depends on your personal situation.

Many experts tend to argue that people need to have an emergency fund comprising three to six months’ worth of living expenses. However, it is not always the case. The choice of the amount depends on personal factors, including your income stability, your household size, your dependants, and how quickly you could find new work if you lost your job.

Here are the personal factors that should shape your target:

You likely need more if you:

- Are self-employed or earn irregular income

- Have children or dependants relying on your income

- Work in a specialised field where finding a new job takes longer

- Have limited or no health insurance

- Are the sole earner in your household

You may be comfortable with less if you:

- Have a highly stable salaried job with strong job security

- Have a dual-income household

- Have very flexible monthly expenses

- Have alternative sources of credit at low cost

The point is not to hit a magic number. The point is to build toward an amount that gives you genuine security in your specific situation.

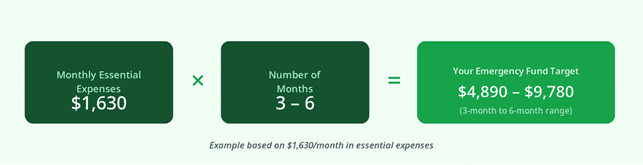

The Simple Emergency Fund Formula

You do not need a calculator to figure out your target. Here is the formula:

Monthly Essential Expenses × Number of Months = Your Emergency Fund Target

Your monthly essential expenses include:

- Rent or mortgage

- Groceries

- Utilities and bills

- Transport

- Insurance

- Loan or debt repayments

- School fees if applicable

Example:

| Expense | Monthly Amount |

| Rent | $800 |

| Groceries | $300 |

| Transport | $150 |

| Utilities | $100 |

| Insurance | $80 |

| Loan repayment | $200 |

| Total | $1,630 |

If your monthly essentials come to $1,630, then:

- A 3-month emergency fund = $4,890

- A 6-month emergency fund = $9,780

That is your target range. You do not need to hit it overnight. The goal is to work toward it consistently, starting with whatever you can set aside right now.

The emergency fund formula in action. Multiply your monthly essential expenses by your target months to get your savings goal.

Is a 3-Month Emergency Fund Enough?

For some people, yes. A 3-month emergency fund is a solid starting point and provides meaningful protection for the most common financial surprises.

A 3-month fund tends to work well if you:

- Have a stable salaried job that is unlikely to disappear suddenly

- Have no dependants or a partner who also earns income

- Have relatively low monthly expenses

- Work in a field where getting a new job typically takes less than a month or two

Think of the 3-month mark as your first real milestone. If you have not started yet, this is the goal to aim for first.

Is a 6-Month Emergency Fund Enough?

For most households, 6 months is the widely recommended standard. It provides a strong enough cushion to cover most scenarios, including a period of unemployment, a significant medical situation, or a combination of smaller expenses hitting at once.

You should aim for 6 months or more if you:

- Are self-employed or earn on a commission or freelance basis

- Have children or other dependants who rely on you

- Work in a specialised role where finding a new position takes time

- Have a single income supporting your household

If you earn irregularly, such as through freelance work or seasonal income, budgeting from your lowest earning month is the safest approach. Our guide on How to Stop Living Paycheck to Paycheck covers irregular income budgeting in more detail.

Where Should You Keep Your Emergency Fund?

There are various means of securing money within the emergency fund. However, they differ regarding convenience and safety. The most reasonable approach is to store your funds in a way that allows easy access to them. Given what an emergency fund is for, these funds cannot be kept in investments that would require much time to liquidate. A savings account or similar option is a better fit.

Here is a breakdown of your best options:

A comparison of the four main options for storing your emergency fund, ranked by suitability. High-yield savings accounts remain the top recommendation for most people globally.

High-Yield Savings Account

This is the most recommended option for most people. A high-yield savings account gives you:

- Easy and fast access to your money

- A competitive interest rate that helps your fund grow

- Safety through FDIC or NCUA insurance (for US-based savers)

Bankrate recommends keeping your emergency savings in an account that offers both a competitive annual percentage yield and easy access. High-yield savings accounts, often offered by online banks, typically offer rates well above standard savings accounts.

The only thing to keep in mind is that transfers to your everyday account may take one to two business days, which is usually fine for most non-immediate emergencies.

Money Market Account

A money market account is similar to a high-yield savings account but often comes with a debit card or the ability to write checks, which makes access even faster. It typically offers a competitive rate and comes with deposit insurance.

This is a good option if you want slightly easier access without sacrificing much in terms of interest.

Standard Savings Account

If you already have a savings account with your bank, it is far better than keeping your emergency fund in your everyday spending account. It creates a clear separation that helps you avoid dipping into the money for things that do not qualify as emergencies.

The downside is that standard savings accounts often pay very little in interest, so your fund does not grow much over time.

Kenya-Specific Options to Consider

If you are based in Kenya, you have a few strong local options worth comparing:

Money Market Funds (MMFs) in Kenya offer relatively liquid access and have historically offered better returns than standard savings accounts. Most MMFs allow same-day or next-day withdrawals, which makes them a practical home for an emergency fund.

SACCOs are another option. They are member-owned and can offer attractive returns, but access to your funds may be slower or subject to specific conditions. For an emergency fund, liquidity matters above almost everything else. If your SACCO does not allow fast withdrawals, it may not be the best fit.

When comparing options, focus on three things: how quickly you can access the money, what the current interest rate is, and whether your principal is protected. Rates on these products change often, so always check directly with the provider before committing.

Should You Invest Your Emergency Fund?

This is a question that often comes up, especially for people who are also trying to grow their wealth. The answer is no, and it is worth understanding why.

Investing your emergency fund, whether in stocks, ETFs, or cryptocurrency, introduces two problems. First, markets go down. If your emergency happens at the same moment the market is down, you may be forced to sell at a loss to cover your costs. Second, most investments take time to liquidate. You may not be able to access the money fast enough when you need it most.

The emergency fund sits in a different category from your investment portfolio entirely. One is for protection. The other is for growth. Mixing the two undermines the purpose of both.

⚠️ Important: Even when markets seem to be performing strongly, your emergency fund should never be invested. The whole point of the fund is that it is there when you need it, regardless of market conditions. As noted by NerdWallet, liquidity and stability matter more than returns for emergency savings.

If you are ready to start investing after building your emergency fund, our guide on Investing for Beginners walks you through exactly how to begin.

When Should You Use Your Emergency Fund?

Knowing when to use your emergency fund is just as important as knowing how to build it.

It is appropriate to use your emergency fund for:

- Job loss and covering essential expenses during unemployment

- Medical or hospital bills that were not anticipated

- Urgent home repairs that affect safety or habitability

- Car repairs required to get to work

- Unexpected travel for a family emergency

It is not appropriate to use your emergency fund for:

- Holidays or discretionary travel

- New gadgets, clothing, or home upgrades

- Planned expenses you simply did not save for

- Investing opportunities, no matter how good they seem

The line to draw is this: if the expense was avoidable with planning, it is not an emergency. If the expense was genuinely impossible to predict and cannot wait, it is.

How to Start Building Your Emergency Fund

Starting from zero can feel overwhelming, especially when the target number seems far away. The key is to focus on the process rather than the destination.

The five-step roadmap for building your emergency fund from zero. Each step builds on the last, and the process works at any income level.

Step 1: Calculate your monthly essential expenses

Use the formula from earlier. Write down everything that must be paid each month and add it up. This becomes your monthly baseline.

Step 2: Set a starter goal

Before targeting 3 or 6 months, aim for your first Ksh 10,000 or $500. A small starter fund still protects you from the most common everyday surprises. It also builds the habit.

Step 3: Open a dedicated account

Keep your emergency fund in a separate account from your everyday spending. Separation makes it easier to track and harder to spend accidentally.

Step 4: Automate a fixed monthly contribution

Set up an automatic transfer to your emergency fund account on the same day your salary arrives. Even a small fixed amount, transferred automatically, builds faster than manual saving.

Step 5: Rebuild it after every use

Most people treat their emergency fund as a one-time savings goal. The moment you draw from it, rebuilding it should immediately become your next financial priority. Put back the money spent so you are prepared for the next emergency.

5 Emergency Fund Mistakes to Avoid

Most individuals fail to use their emergency funds correctly. The majority treat this fund as additional savings that can be used freely. These five mistakes are the most common ones worth watching out for.

Mistake 1: Using it for non-emergencies

A sale, a spontaneous trip, or an upgrade that “seemed like a good deal” are not emergencies. Every time you draw from this fund for a non-emergency, you lose protection for the real ones.

Mistake 2: Keeping it in your everyday account

If your emergency fund lives in the same account as your groceries and entertainment spending, it will disappear. Keep it separate.

Mistake 3: Investing it in stocks or crypto

As covered above, investing your emergency fund exposes it to market risk and liquidity delays. This is one of the most common and costly mistakes people make.

Mistake 4: Never rebuilding it after use

Using the fund for a genuine emergency is exactly right. But most people do not replenish it afterward. Your fund should always be working toward its full target.

Mistake 5: Saving too little or too much

Too little leaves you exposed. But keeping excessively more than 6 to 9 months of expenses in a low-interest account when that money could be working harder in investments is also a missed opportunity. The goal is the right amount, not an infinitely growing one.

The Federal Reserve’s Report on the Economic Well-Being of U.S. Households consistently finds that a significant proportion of adults would struggle to cover an unexpected $400 expense — a powerful reminder of how widespread these gaps in preparation truly are.

Emergency Fund vs Savings Account: What Is the Difference?

These two things are often confused, but they serve different purposes.

| Emergency Fund | Savings Account | |

| Purpose | Unexpected financial emergencies only | Any savings goal, planned or unplanned |

| Access | Available immediately when needed | Available, but may be used for goals |

| Mental framing | Off-limits unless it is a true emergency | Flexible, goal-driven |

| Ideal location | Separate account, ideally high-yield | Can be same account as other savings |

| Target amount | 3 to 6 months of essential expenses | Depends on the goal |

The emergency fund is a subset of your broader savings. It is the part you do not touch no matter what, reserved exclusively for genuine crises. Everything else you save for, including a holiday, a car, or a home deposit, belongs in separate buckets.

Personal Perspective

Personally, I view an emergency fund as the foundation of financial security. Before focusing on investing or building wealth, I believe it is important to have a financial cushion that can absorb unexpected expenses. In my experience, the peace of mind that comes from knowing money is available for emergencies is just as valuable as the money itself. An emergency fund reduces financial stress, helps avoid unnecessary debt, and makes it easier to stay focused on long-term financial goals.

Frequently Asked Questions

What is an emergency fund?

An emergency fund is a dedicated amount of money saved exclusively to cover unexpected financial situations, such as job loss, medical bills, or urgent repairs. It is separate from your everyday savings and investments.

How much money should you have in an emergency fund?

Most financial experts recommend saving between 3 and 6 months of your essential monthly expenses. The right amount for you depends on your income stability, household size, and job security.

Is a 3-month emergency fund enough?

For individuals with stable employment and no dependants, a 3-month fund provides meaningful protection. It is also an excellent starting milestone for anyone who is just beginning to build their fund.

Is a 6-month emergency fund enough?

For most households, especially those with dependants, irregular income, or a single earner, 6 months is the recommended standard. Some households choose to save more depending on their circumstances.

Where should I keep my emergency fund?

A high-yield savings account is the most recommended option. It offers easy access, a competitive interest rate, and deposit insurance. A money market account is another strong choice. For Kenyan readers, a well-rated money market fund can also work well.

Should I invest my emergency fund?

No. Investments carry market risk and may not be accessible quickly enough in a genuine emergency. Keep your emergency fund in a liquid, protected account separate from your investment portfolio.

What is an emergency fund used for?

It is used for genuinely unexpected expenses: sudden job loss, unexpected medical costs, urgent home or car repairs, and unplanned crises that could not have been saved for in advance.

When should I use my emergency fund?

Only when faced with a true financial emergency that is unexpected, necessary, and urgent. Non-emergency spending should always come from your regular budget.

What is the most common mistake made with emergency funds?

Using the fund for non-emergencies and failing to rebuild it afterward are the two most common mistakes. Setting it and forgetting it is a close third.

Is an emergency fund the same as a savings account?

No. A savings account is a tool. An emergency fund is a dedicated purpose. You can keep your emergency fund in a savings account, but not every savings account is an emergency fund.

Where can I save an emergency fund in Kenya?

Popular options include money market funds offered by fund managers, savings accounts with commercial banks, and in some cases SACCOs. Prioritise liquidity and access speed when choosing.

Conclusion

Building an emergency fund is one of the most important financial decisions you will ever make. Not because it is exciting, but because it protects everything else you are working toward.

I think that having an emergency fund is extremely important before making investments or accumulating more wealth in any way. Without it, every financial goal you set is one unexpected event away from being derailed.

Start with what you can. Even setting aside a small amount this month puts you ahead of where you were. Use the formula to find your target. Choose the right account. Set up an automatic contribution. And remember: the moment you use the fund, rebuilding it becomes your next priority.

Your emergency fund is not just money sitting in an account. It is the foundation that makes every other financial goal possible.

Ready to take your next step?

Check out our guide on how to build the habits that make saving easier every month.

How to Stop Living Paycheck to Paycheck →

Disclaimer: This content is for informational and educational purposes only. It does not constitute financial advice. Always consult a qualified financial advisor before making financial decisions.