I still remember the moment compound interest stopped being a textbook concept and became very real to me. It was a modest amount that helped me move on. A couple of years later, I checked my account and noticed that it had grown not because of my contributions but thanks to the earnings. In other words, an almost invisible process taking place behind the scenes is what makes up compound interest. And once you realize its power, nothing else matters anymore.

If you have ever wondered why some people seem to grow their wealth steadily without doing anything dramatic, compound interest is usually the answer. It is not luck. It is not a secret investment tip. It is a mathematical principle that quietly rewards those who start early and stay consistent.

In this guide, we will break down exactly what compound interest is, how it works, and why starting at 25 gives you a massive advantage over starting at 35 — with real numbers to prove it.

1. What Is Compound Interest? (Plain English Definition)

Compound interest is the interest you earn on both your original principal and the interest that has already been added to your account. In simple terms: you earn interest on your interest.

Here is the simplest way to think about it. Imagine you plant a tree. Every year, the tree grows branches. The following year, those branches also grow new branches. Over time, you have not just one tree — you have an entire forest, all from a single seed. That is compound interest.

This is fundamentally different from simple interest, where you only earn returns on your original amount. With compound interest, your money is always growing — and the growth accelerates the longer you leave it.

2. Simple Interest vs Compound Interest: A Quick Comparison

Before diving into the numbers, it helps to understand how these two types of interest differ.

| Feature | Simple Interest | Compound Interest |

| Calculated on | Original principal only | Principal + accumulated interest |

| Growth type | Linear (steady, flat) | Exponential (accelerating) |

| Best for | Short-term loans | Long-term investing |

| Example (10 years, 8%) | $8,000 interest on $10,000 | $11,589 interest on $10,000 |

| Common use | Car loans, some personal loans | Savings accounts, index funds, ETFs |

The difference looks small in year one. But as the years compound, the gap becomes enormous — and that is precisely the point.

3. How to Calculate Compound Interest

The compound interest formula is:

A = P(1 + r/n)^(nt)

Where:

- A = Final amount (principal + interest)

- P = Principal (your initial investment)

- r = Annual interest rate (as a decimal, so 8% = 0.08)

- n = Number of times interest compounds per year

- t = Time in years

For example, if you invest $10,000 at 8% interest compounded annually for 20 years:

A = 10,000 × (1 + 0.08/1)^(1×20) = $46,609

That is $36,609 in interest earned on a $10,000 investment — nearly four times your money, without touching it. You can use a compound interest calculator to run your own scenarios.

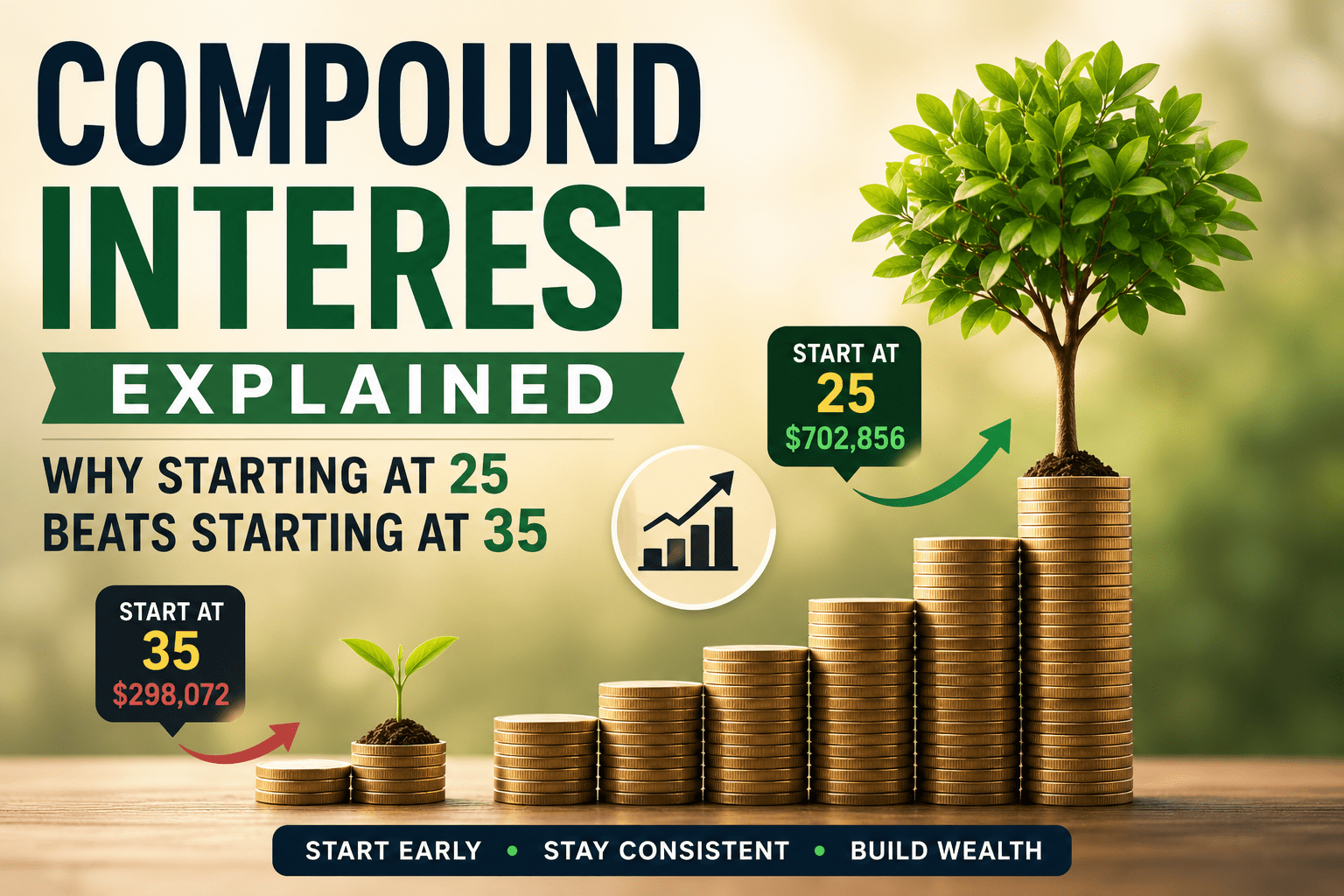

4. Real-Money Example: Starting at 25 vs Starting at 35

This is where it gets powerful. Let us compare two investors — both investing $200 per month at an average annual return of 8%.

| Investor A (Starts at 25) | Investor B (Starts at 35) | |

| Monthly investment | $200 | $200 |

| Start age | 25 | 35 |

| Retirement age | 65 | 65 |

| Years invested | 40 years | 30 years |

| Total contributed | $96,000 | $72,000 |

| Final balance at 65 | $702,856 | $298,072 |

| Extra gained | +$404,784 | — |

Investor A ends up with over $400,000 more — despite only contributing $24,000 more. That extra decade of compounding made all the difference.

Figure 1. Compound interest comparison using $200 monthly contributions and an 8% average annual return.

In terms of finance expertise, it should be noted that people who managed to save money at some point, despite the sums being saved, do have much greater freedoms compared to those who failed to do that. Again, there is no question of people’s ability to earn or show more intelligence, which is the case. The only thing that makes these people different from one another is the time.

5. The Two Levers: Time and Rate of Return

Compound interest has two powerful drivers you can influence:

Time

Time is the single most important ingredient. The earlier you start, the more compounding cycles your money goes through. Even a few extra years at the beginning creates a dramatically different outcome at the end, as the example above shows.

Rate of Return

The higher your annual return, the faster your money grows. Historically, a diversified index fund has returned an average of 7–10% per year over long periods. Even a 1–2% difference in return compounds to a massive gap over 30+ years.

This is why choosing the right investment vehicle matters. A savings account giving you 2% will compound — but it will do so far slower than an index fund averaging 8%. Both use compound interest, but the rate of return separates the outcomes.

6. The Rule of 72: A Mental Shortcut Every Investor Needs

The Rule of 72 is one of the most useful quick-math tools in personal finance. Here is how it works:

Years to double your money = 72 ÷ Annual Interest Rate

So at an 8% return, your money doubles roughly every 9 years. At 6%, it takes 12 years. At 12%, just 6 years.

Figure 2. The Rule of 72 shows how the rate of return changes the time needed to double your money.

This rule helps you quickly evaluate investment options and understand the long-term cost of low-return savings products. It is also why high-interest debt is so dangerous — a credit card charging 24% interest will double what you owe in just 3 years.

7. The 8-4-3 Rule of Compounding

Many investors are familiar with the Rule of 72, but fewer know about the 8-4-3 rule. This rule describes the acceleration pattern of compound interest over time:

- Your investment takes 8 years to double for the first time

- It doubles again in just 4 more years

- And doubles again in 3 more years

This is the exponential nature of compounding in action. The later years do the heavy lifting. If you pull out your money early, you miss the period where compounding truly accelerates. Patience is not optional — it is the strategy.

8. Where Compound Interest Works For You

Here are the main places where compound interest builds your wealth:

Index Funds and ETFs

In all honesty, index funds helped me to see compound interest in action for the very first time. There is no need for any special knowledge or effort here since all that matters is constancy. The only disadvantage that can be named is the lack of appeal.

Index funds are one of the most accessible and effective vehicles for compound growth. They track a market index (like the S&P 500), spread your risk across hundreds of companies, and deliver average returns of 7–10% annually over the long run. For a full breakdown, read What Is an Index Fund and Why Most Experts Recommend It.

ETFs (Exchange-Traded Funds)

ETFs work similarly to index funds but are traded on stock exchanges. They offer flexibility, low fees, and consistent exposure to market returns. If you are choosing between the two, check out ETFs vs Mutual Funds: Which Is Better for a Beginner Investor? for a detailed comparison.

Retirement Accounts (Roth IRA, 401k)

Tax-advantaged accounts like a Roth IRA allow your investments to compound without being reduced by taxes each year. This significantly accelerates growth. Learn whether to open a Roth IRA vs. Brokerage Account as a beginner.

High-Yield Savings Accounts

While returns are lower than stock market investments, high-yield savings accounts still use compound interest. They are ideal for emergency funds or short-term goals where you cannot afford market volatility.

9. Where Compound Interest Works Against You

Compound interest is a double-edged sword. When it works against you — typically in the form of debt — it is just as powerful, but in a destructive direction.

Credit Card Debt

Most credit cards charge interest rates between 20–30% annually, compounded monthly. If you carry a balance of $5,000 at 24% APR and make only minimum payments, you could end up paying back more than double your original balance.

Student Loans and Personal Loans

Many loans compound interest daily or monthly. A loan that seems manageable at first can grow significantly if not paid down aggressively. Understanding which loans are compound interest is critical before you sign anything.

The lesson: use compound interest to build wealth, and aggressively eliminate compound interest debt. The same mathematical force that builds your portfolio can quietly drain it if you are on the wrong side of it.

10. The Best Investments for Compound Interest

Not all investment vehicles are equally effective for compounding. Here is a ranked overview:

- Index funds and ETFs — Low cost, diversified, long track record of 7–10% annual returns

- Dividend reinvestment stocks — Reinvesting dividends creates compounding within individual stocks

- Roth IRA / 401k — Tax-advantaged growth amplifies compounding significantly

- High-yield savings accounts — Lower returns but safe and liquid

- Bonds — Stable but lower-growth compounding, better for conservative portfolios

The common thread: the best compound interest investments are ones you can leave alone for years. Passive income strategies that pair well with compounding include dividend stocks and REITs — explore Passive Income Ideas for Beginners in 2026.

11. How to Start Today — Even With a Small Amount

One of the biggest myths about investing is that you need a large sum to get started. You do not. Compound interest does not care how much you start with — it cares how long you leave it.

Here is a practical starting plan:

- Free up money to invest — Start by building a budget that creates room for consistent monthly contributions. Read How to Build a Monthly Budget That Actually Works.

- Open an investment account — A brokerage account or Roth IRA gives you access to index funds and ETFs.

- Choose a low-cost index fund — Look for funds with low expense ratios (under 0.2%) that track a broad market index.

- Set up automatic contributions — Automating your investments removes emotion and ensures consistency.

- Leave it alone — This is the hardest part. Resist the urge to sell during market dips. Time in the market beats timing the market.

If you are ready to begin, Investing for Beginners: What to Do With Your First $1,000 is the best place to start.

And if you want to build the habits that make wealth-building sustainable, The 7 Habits of People Who Build Wealth From Scratch is a must-read.

12. Frequently Asked Questions

What will $100 become after 20 years at 5% compound interest?

At 5% compounded annually, $100 grows to approximately $265 after 20 years. The formula gives: 100 × (1.05)^20 = $265.33.

Figure 3. A small amount can grow meaningfully when compound interest has enough time to work.

Is 1% per month the same as 12% per year?

No — and this is a common misconception. Because of compounding, 1% per month is actually equivalent to about 12.68% per year (calculated as (1.01)^12 − 1). Always check whether a rate is monthly or annual before comparing.

What is the best age to start investing?

The best age to start is as early as possible. Even investing small amounts in your early 20s will outperform larger amounts invested in your 30s, due to the power of time in the compound interest formula.

Which loans use compound interest?

Most credit cards, student loans, mortgages, and personal loans use compound interest. Always check the compounding frequency (daily, monthly, annually) when evaluating any loan product.

What creates 90% of millionaires?

According to various studies, the majority of millionaires built wealth through consistent, long-term investing — particularly in real estate and diversified stock portfolios. The common factor is time in the market and the power of compound interest, not high incomes or lucky stock picks.

Final Thoughts

What needs to be mentioned here is that compound interest is favorable to those who show patience but hostile to those who procrastinate. Just do your homework!

Compound interest is not a get-rich-quick scheme. It is a get-rich-slowly, surely, and reliably strategy. The earlier you start, the more powerfully it works in your favour. The later you wait, the more you are working against yourself.

Whether you are 22 or 42, the best time to start is now. Open that account. Set up that automatic investment. Choose a simple, low-cost index fund. And then leave it alone.

Your future self will thank you.

Ready to put compound interest to work? Start here:

→ Investing for Beginners: What to Do With Your First $1,000

Subscribe to the MoneyMapJournal newsletter for weekly money tips delivered straight to your inbox.