ETFs vs Mutual Funds — if you’ve ever Googled “how to start investing”, chances are the very first decision that stopped you in your tracks was this: the ETFs vs Mutual Funds debate. Both terms get thrown around constantly in personal finance, and for good reason — both are excellent vehicles for building long-term wealth.

But ETFs vs Mutual Funds are not identical, and for a beginner with limited capital, the differences matter. This guide breaks everything down — how each works, where each wins, and most importantly, which one you should choose first.

And if you’re still figuring out the basics, read our guide on Investing for Beginners: What to Do With Your First $1,000 before continuing here.

| 📖 Start Here — MoneyMapJournal Investing for Beginners: What to Do With Your First $1,000 → |

Key investing statistics — moneymapjournal.com

— The Basics —

What Are ETFs and Mutual Funds?

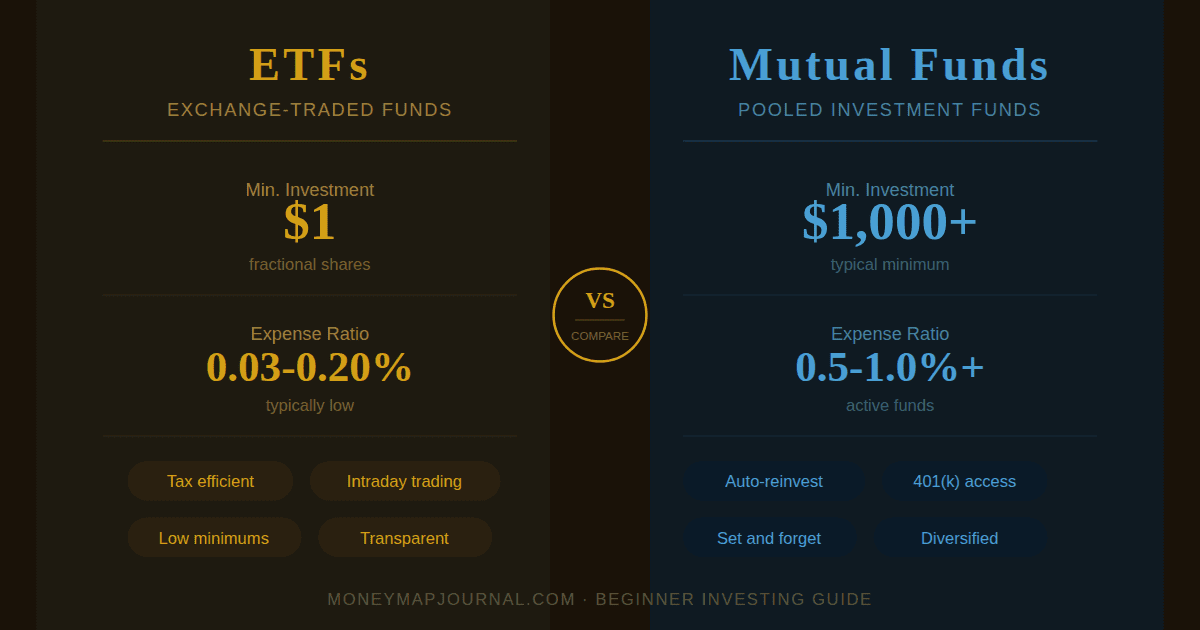

Exchange-Traded Funds (ETFs)

An exchange-traded fund (ETF) is an investment product that holds a basket of underlying assets — stocks, bonds, commodities, or a mix. It trades on a stock exchange throughout the day, exactly like shares in a company. When you buy one ETF share, you’re instantly invested in every asset that ETF holds.

According to the U.S. Securities and Exchange Commission (SEC), ETFs must register as open-end investment companies under the Investment Company Act of 1940. The first U.S. ETF was the SPDR S&P 500 ETF (SPY), launched in January 1993 — and it remains the most traded ETF in the world today.

Mutual Funds

A mutual fund also pools money from many investors to buy a diversified portfolio. However, unlike ETFs, mutual fund shares cannot be traded during market hours. Shares are priced just once per day, after markets close, at the fund’s Net Asset Value (NAV).

According to Investopedia, mutual fund investment has grown from about 6% of U.S. households in 1980 to 54% in 2025 — making them the single most popular investment vehicle for American households. For most people, the first encounter with mutual funds is through a workplace 401(k) plan.

Mutual funds give everyday investors access to a diverse investment menu they likely couldn’t build on their own. Investing in a single stock or bond can be risky, but a mutual fund reduces the risk by spreading investments across many securities.

— The Key Differences —

ETFs vs Mutual Funds: Side-by-Side Comparison

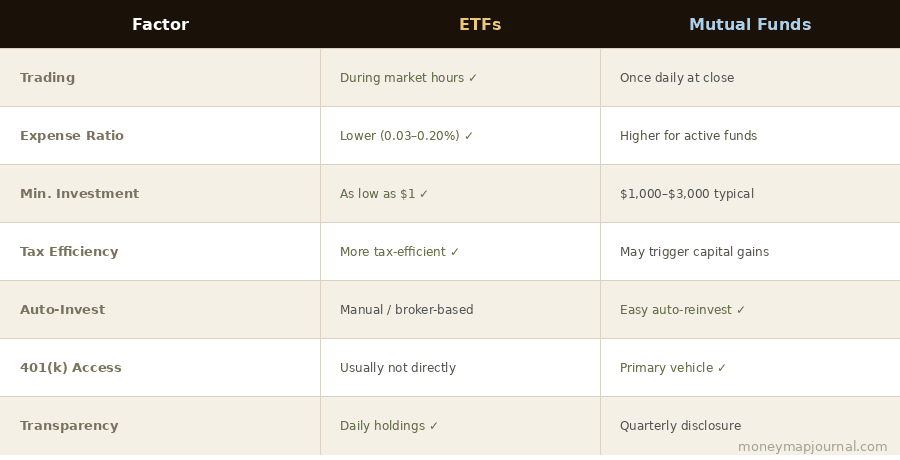

Here are the eight most important ETFs vs Mutual Funds factors every beginner investor should understand before choosing:

| Factor | ETFs | Mutual Funds |

| Trading | Anytime during market hours | Once daily after close |

| Pricing | Real-time throughout the day | End-of-day NAV only |

| Expense Ratios | Generally lower (0.03–0.20%) | Higher for active funds |

| Min. Investment | As low as $1 | $1,000–$3,000 typical |

| Tax Efficiency | More tax-efficient | May trigger capital gains |

| Auto-Invest | More complex to set up | Easy auto-reinvestment |

| 401(k) Access | Not typically available | Primary 401(k) vehicle |

| Transparency | Daily holdings disclosed | Quarterly disclosure |

ETFs vs Mutual Funds comparison — moneymapjournal.com

Note: ✓ marks indicate where each option has a meaningful advantage. For a deeper dive into index funds — which are available as both ETFs and mutual funds — read our guide: What Is an Index Fund and Why Most Experts Recommend It.

| 📈 Related — MoneyMapJournal What Is an Index Fund and Why Most Experts Recommend It → |

Cost: The Biggest Factor for Long-Term Returns

Fees are the silent wealth killer. A difference of just 0.5% per year in annual fees can cost you tens of thousands of dollars over a 30-year investing horizon. This is where ETFs vs Mutual Funds diverge most clearly — and where ETFs often hold a real edge.

Because most ETFs passively track an index — like the S&P 500 — they require less active management, translating into dramatically lower expense ratios:

| 💰 Real-World Cost Comparison Vanguard 500 Index Fund (VFIAX) — mutual fund, 0.04% expense ratio, $3,000 minimumFidelity 500 Index Fund (FXAIX) — mutual fund, 0.015% expense ratio, no minimumSPDR S&P 500 ETF (SPY) — ETF, ~0.095% expense ratio, no minimum beyond share priceT. Rowe Price Dividend Growth Fund (PRDGX) — actively managed mutual fund, 0.64% expense ratio |

The real lesson: passive index funds beat actively managed funds on cost regardless of whether they’re structured as ETFs or mutual funds. The ETF vs mutual fund cost debate largely disappears when you compare passive-to-passive. Where ETFs clearly win is against actively managed mutual funds, which charge up to 10× more.

Tax Efficiency: Why ETFs Have a Structural Edge

This matters most if you’re investing in a taxable brokerage account (rather than a 401(k) or Roth IRA).

When you sell mutual fund shares, the fund may need to sell underlying securities to give you your cash back. This can trigger capital gains events that every shareholder must pay — even those who didn’t sell anything. ETFs avoid this entirely through in-kind creation and redemption: authorized participants exchange baskets of stocks directly for ETF shares, generating far fewer taxable events.

An ETF is more tax-efficient than a mutual fund because most buying and selling occurs through an exchange, and the ETF sponsor doesn’t need to redeem shares each time an investor wishes to sell.

Bottom line: if you’re investing in a taxable brokerage account, the ETFs vs Mutual Funds tax efficiency gap is a meaningful long-term advantage for ETFs. If you’re investing through a 401(k) or Roth IRA, this difference is largely irrelevant — both work equally well.

| 🏦 Related — MoneyMapJournal Roth IRA vs. Brokerage Account: Which Should Beginners Open First? → |

ETFs vs Mutual Funds: Types Every Beginner Should Know

Index Funds (ETF or Mutual Fund)

The single best starting point for most beginner investors navigating the ETFs vs Mutual Funds decision. Index funds passively track a market benchmark like the S&P 500. They require minimal management, charge the lowest fees, and historically outperform most actively managed funds over the long run. Available as both ETFs and mutual funds.

Target-Date Funds (Usually Mutual Funds)

The ultimate “set it and forget it” option. Choose a fund named after your target retirement year (e.g., “2055 Fund”) and the fund automatically shifts from aggressive growth to conservative investments as you approach retirement. Over 90% of U.S. employer retirement plans use these as their default investment. Excellent for beginners who want zero maintenance.

Bond Funds (ETF or Mutual Fund)

Bond funds invest in fixed-income securities like government or corporate bonds. They provide steady income and help balance out stock market volatility. Beginners building a diversified portfolio often pair a stock index ETF with a bond fund.

Actively Managed Funds (Usually Mutual Funds)

A fund manager actively picks stocks and makes daily buy/sell decisions, attempting to beat the market. These charge significantly higher fees and the majority fail to outperform their benchmark index over the long term. Not recommended as a starting point for beginner investors.

How to Earn Money from ETFs and Mutual Funds

Both ETFs vs Mutual Funds vehicles generate returns through the same three mechanisms:

| 📊 Three Ways You Earn Returns Dividends: Income from stocks (dividends) or bonds (interest) held in the portfolio, passed on to you as a distribution.Capital Gains Distributions: When the fund sells securities at a profit, those gains are distributed to shareholders.Price Appreciation: As the market value of the fund’s holdings rises, the ETF market price or mutual fund NAV increases — and so does your investment. |

One practical difference: with mutual funds, dividend reinvestment is seamless — you elect to reinvest and fractional shares are added automatically. With ETFs, reinvesting dividends may require a manual step or depend on your broker’s fractional share support.

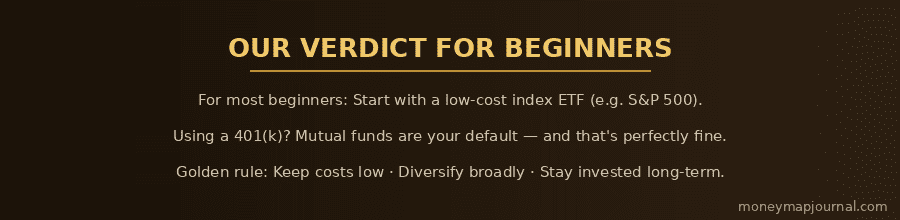

Our Conclusion: Which Should a Beginner Choose?

After comparing ETFs vs Mutual Funds across costs, tax efficiency, trading flexibility, minimum investment requirements, and beginner-friendliness, here is our honest, practical verdict.

| 🏆 FINAL VERDICT: Our Recommendation for Beginner Investors ▶ Start with a low-cost index ETF if you’re opening a brokerage account. For most beginners opening their first investment account today, a broad market index ETF — like one tracking the S&P 500 (SPY, VOO, or IVV) — is the ideal starting point. You can begin with as little as $1 on many platforms, fees are near zero, and you get instant diversification across 500 of the world’s largest companies in a single purchase. ▶ Use mutual funds if you’re investing through a 401(k). If your first investing experience is through an employer-sponsored retirement plan, you will almost certainly be working with mutual funds — and that is perfectly fine. A low-cost target-date mutual fund inside a 401(k) is an excellent, set-and-forget investment. Always contribute at least enough to capture your employer’s full match: that is an instant 50–100% return on your contribution. ▶ Consider holding both as your portfolio grows. Many seasoned investors hold ETFs vs Mutual Funds simultaneously — mutual funds in their 401(k) and ETFs in a separate taxable brokerage account. This combination gets you the best of both worlds: tax-advantaged retirement growth through mutual funds, and tax-efficient flexibility through ETFs. There is no rule against using both. ▶ Above all: start now, start simple, keep costs low. The single biggest investing mistake beginners make is waiting for the “perfect” choice. Whether you start with an ETF or a mutual fund, time in the market consistently outperforms timing the market. A $5,000 investment in a low-cost index fund today — left to grow for 30 years at an average 8% return — grows to approximately $50,000. Start with what’s available to you, keep costs low, diversify broadly, and stay the course. |

Practical First Steps: How to Get Started Today

Here is a simple, actionable roadmap to start investing in ETFs or mutual funds this week:

- Check your employer’s 401(k). If there’s an employer match, always contribute enough to capture it first — it’s the highest guaranteed return you’ll find anywhere.

- Open a brokerage account. Fidelity, Vanguard, and Charles Schwab are the most beginner-friendly for mutual funds. For ETFs, any major online broker or app (Robinhood, Webull) works.

- Pick one low-cost index fund and buy it. Don’t overthink it. A single S&P 500 index ETF or mutual fund is sufficient to start. You can diversify further as your portfolio grows.

- Set up automatic monthly contributions. Automate your investing. Even $50–$100/month builds significant wealth over 20–30 years through compound growth.

- Read the fund prospectus. Free on the SEC website. Confirm fees, holdings, and strategy before you commit.

- Review quarterly — but don’t obsess. Check your portfolio every 3 months. Resist the urge to react to short-term market swings.

Not sure how to fit investing into your monthly budget? Read our guide: How to Build a Monthly Budget That Actually Works — it shows you exactly how to find investable money every month, even on a tight income.

| 📊 Related — MoneyMapJournal How to Build a Monthly Budget That Actually Works (Zero-Based Method) → |

| 💰 Related — MoneyMapJournal Passive Income Ideas for Beginners in 2026: 15 Ideas That Actually Work → |

— FAQs —

Frequently Asked Questions

Are ETFs safer than mutual funds?

Neither is inherently safer. In the ETFs vs Mutual Funds debate, both carry market risk. The risk level depends on what the fund holds, not on whether it is structured as an ETF or mutual fund. A broad index fund of either type is generally lower risk than a concentrated sector fund.

Can I invest in both ETFs and mutual funds?

Yes, and many investors do. The ETFs vs Mutual Funds choice doesn’t have to be exclusive — a common approach is mutual funds inside a tax-advantaged 401(k), and ETFs inside a taxable brokerage account. There is no penalty or restriction on holding both simultaneously.

How much money do I need to start?

Some ETFs can be purchased for as little as $1 through fractional shares on platforms like Fidelity or Robinhood. Most ETFs have no minimum beyond their share price. Many mutual funds require $1,000 to $3,000 minimum, though some — like the Fidelity ZERO funds — have no minimum at all.

Is an index fund an ETF or a mutual fund?

An index fund is a strategy — not a structure. It can be implemented as either an ETF or a mutual fund. Both Vanguard’s VOO (an ETF) and its VFIAX (a mutual fund) track the S&P 500. See our full guide: What Is an Index Fund and Why Most Experts Recommend It.

Are ETFs guaranteed by the government?

No. ETFs and mutual funds are not insured by the FDIC or any government agency. You can lose money. However, your brokerage account is protected by SIPC (Securities Investor Protection Corporation) for up to $500,000 if your broker fails.

⚠️ DISCLAIMER

This article is for educational and informational purposes only. It does not constitute financial advice. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Always consult a qualified financial advisor before making investment decisions.