Raising financially independent children is one of the most important — and most overlooked — gifts you can give your kids. Money management is not something most schools teach, which means the responsibility falls squarely on us as parents. I have come to realize that if I want my children to grow up making smart money decisions, I need to start the conversation early, long before they ever hold their first paycheck.

In this guide, I walk you through exactly how to raise financially independent children from toddler to teen — with practical, age-by-age strategies that actually work in real life. Whether your child is three years old or fifteen, there is something here for every stage of the journey.

“Do not save what is left after spending; spend what is left after saving.” — Warren Buffett

Why Teaching Financial Independence Early Matters

Here is a sobering statistic: only 16% of adults aged 18 to 24 are fully financially independent. That means the vast majority of young adults are still leaning on their parents for rent, groceries, or emergency support well into adulthood. I do not want that for my children — and I suspect you don’t want it for yours either.

The good news? The habits that lead to financial independence are not complicated. They are built slowly, over years, through consistent exposure to real money concepts. The earlier you start raising financially independent children, the more natural these habits become. You can read more about age-specific approaches on our sister guide on Teaching Kids About Money: An Age-by-Age Guide.

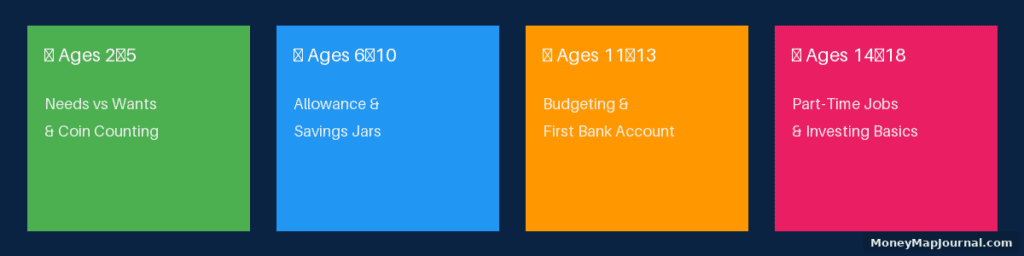

Figure 1: Four key stages of raising a financially independent child

Ages 2–5: Planting the First Seeds

Start With Needs vs. Wants

To raise financially independent children, you must start early — even before they can count. Toddlers and preschoolers can grasp far more than we give them credit for. I started talking to my children about money while doing the most mundane things — grocery shopping, paying bills, running errands. When my four-year-old pointed at a toy in the supermarket, instead of just saying no, I explained: “That’s a want, not a need. We need food first.”

These small moments build foundational money thinking. Use simple language: food, clothes, and a home are needs. Toys, sweets, and new shoes are wants. Repetition is everything at this age.

Introduce Coins and Notes

Let your child handle real money. Let them count coins. Let them give money to the cashier and receive change. The physical act of exchanging money makes it concrete in their minds — far more than an abstract lesson ever will.

Tip: A clear glass jar works better than a piggy bank for toddlers. They can see the money growing, which makes saving exciting and visual.

Ages 6–10: Building the Money Habit

Give an Allowance — and Make It Meaningful

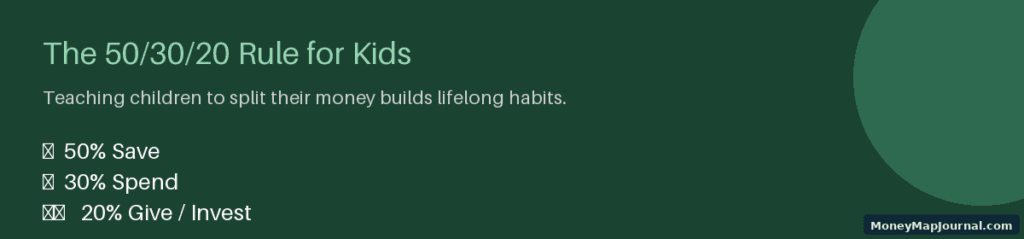

One of the best decisions I made was starting a structured allowance system for my children around age six. A structured allowance is one of the most effective tools for raising financially independent children at this stage. An allowance is not charity — it’s a teaching tool. The key is to tie it to a system, not just hand out money freely. For a full breakdown of how much to give at each age, check out our Complete Kids Allowance Guide.

Here is the system I recommend and use:

- Save 50% — into a savings jar or bank account

- Spend 30% — for small, personal purchases they choose

- Give/Invest 20% — for charity, gifts, or a family savings goal

This 50/30/20 rule, adapted for children, is powerful because it teaches allocation before they ever earn a real salary. When they internalise this at age seven, managing a payslip at twenty-five becomes instinctive.

Figure 2: The 50/30/20 money split rule for children

Open a Real Savings Account

By age eight or nine, your child is ready for a real bank account. Take them with you to open it. Let them fill in the forms (or at least watch). Have them make their own deposits — even if it’s just $1. This sense of ownership is what turns a passive child into an active saver — and active savers grow into financially independent children.

Many banks and credit unions offer junior savings accounts with no monthly fees and small minimum balances. The interest may be small, but the lesson is priceless. Speaking of building savings habits, our article on Emergency Funds: How Much You Really Need and Where to Keep It is a great resource to share with older children transitioning to more serious savings.

Ages 11–13: Building Financial Literacy

Teach Them to Budget

At the preteen stage, raising financially independent children means introducing them to the mechanics of a budget. I invite my children to watch — and eventually participate — when I sit down to plan our household spending. They see how much food costs. They see the electricity bill. They understand that money is finite.

A great entry point is to give your preteen a small budget for a specific expense — their school lunch for the week, or money for a class trip — and let them manage it. If they run out early, resist the urge to top them up. That moment of running out of money is one of the most educational experiences a child can have. You can also use our Monthly Budget Template guide as a starting framework to adapt for your child.

Explain How Credit and Debt Work

Preteens are old enough to understand that credit cards are not free money. Show them a real statement (blurring out sensitive details if needed). Explain: “Every time I swipe this card, I’m borrowing money. If I don’t pay it back in full, I owe extra — that’s called interest.”

This is also a good time to introduce the concept of compound interest — but in a positive framing. Our article on Compound Interest: Why Starting at 25 Beats Starting at 35 uses simple, visual examples you can literally read together with your 12-year-old.

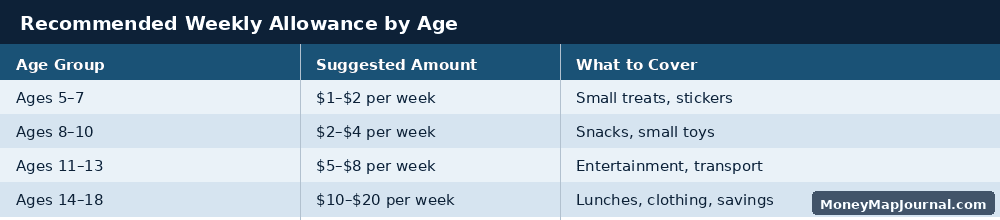

Figure 3: Recommended weekly allowance guide by age group

Ages 14–18: Earning, Investing, and Independence

Require Teenagers to Earn Their Spending Money

This is the stage where financially independent children begin to develop a real work ethic. A part-time job — whether it is tutoring, pet-sitting, selling crafts, or helping a neighbour — teaches more than any classroom lesson ever could.

Earning their own money does three things for your teenager:

- It makes them value money more — because they know exactly how many hours it took to earn it.

- It teaches them that lifestyle is earned, not inherited — linking effort to reward.

- It builds confidence and independence that goes far beyond money management.

Encourage them to automate saving — set up an automatic transfer of part of every income into a savings or investment account. This mirrors what financially successful adults do, and our guide on stopping the paycheck-to-paycheck cycle shows exactly how that habit plays out in adult life.

Introduce Investing — Even With Small Amounts

Teenagers can and should start learning about investing. The magic of compound interest means that $50 invested at 16 will be worth far more than $500 invested at 30. Open a custodial investment account with your teen, make a small investment together, and track it monthly. Discuss the ups and downs. This experience will shape how they manage money for the rest of their lives.

For parents who want to explain the basics of investing to their teens, our article comparing ETFs vs Mutual Funds for Beginners is an excellent, jargon-free starting point. And for teens already thinking about passive income streams, our Passive Income Ideas for Beginners guide opens up a world of possibilities.

Have an Honest Conversation About the Future

Before your teenager leaves home, have a frank money conversation. Discuss: How much support will you provide during university? What happens after they graduate? What do you expect them to pay for themselves, and by when? Financial independence does not happen accidentally — it is planned for.

Help your teen build a basic budget for the life they want to live. If their career path cannot support that lifestyle right away, help them understand the trade-offs and timelines involved. This is not about discouragement — it is about reality, and reality is a kindness.

Key Mistakes Parents Make (And How to Avoid Them)

Even the most well-intentioned parents can accidentally undermine their children’s financial independence. Here are the most common pitfalls I have seen — and personally had to correct:

- Always bailing them out. When your child spends their allowance and has nothing left, let them feel that. The discomfort is the lesson.

- Never talking about money openly. Children who grow up in homes where money is a taboo topic enter adulthood financially illiterate.

- Giving allowances with no structure. Money without purpose teaches nothing. Tie allowances to saving goals and spending categories.

- Doing everything for them. Let teenagers manage their own phone top-up, their own school supplies budget, their own savings transfers. Doing it for them robs them of the skill.

One external resource I find genuinely useful for parents is the Practical Money Skills platform by Visa, which offers interactive guides and games for children of all ages. It complements the conversations you are already having at home.

Final Thoughts: Start Where You Are

The most important thing about raising financially independent children is not having a perfect system — it’s starting. Even if your child is already twelve and has never had an allowance or a savings account, it is not too late. Start today. Open that account. Have that conversation. Give them a small budget to manage.

Every conversation you have about money, every savings jar you set up, every payslip you walk them through — it adds up. These small, consistent actions are the foundation of financially independent children. And one day, when your child calls you to say they have built their emergency fund, or made their first investment, or negotiated their salary with confidence, you will know exactly where those habits came from.

You built them. One lesson at a time. For more practical strategies on building wealth and managing money wisely, explore our Building Wealth category and the full For Parents resource hub right here on MoneyMapJournal.com